I have been preparing a new Wikipedia page for financialization. It is startling that there is no such page yet, seeing as how financialization has been one of the most important and most powerful trends of the past three decades. Here is what I have so far:

Financialization is a relatively new term used increasingly to discuss the emergence of a new form of capitalism in which financial markets dominate over the traditional industrial economy. Greta Krippner of the University of California - Los Angeles has written that "financialization" refers to a "pattern of accumulation in which profit making occurs increasingly through financial channels rather than through trade and commodity production." Some scholars have insisted on a much more narrow use of the term: the ascendancy of "shareholder value" as a mode of corporate governance; or the growing dominance of capital market financial systems over bank-based financial systems.

More downstairs ...

More popularly, however, financialization is understood to mean the vastly expanded role of financial motives, financial markets, financial actors and financial institutions in the operation of domestic and international economies. In his 2006 book, American Theocracy: The Peril and Politics of Radical Religion, Oil, and Borrowed Money in the 21st Century, American writer and commentator Kevin Phillips defined financialization as "a process whereby financial services, broadly construed, take over the dominant economic, cultural, and political role in a national economy." (page 268). Philips warns that the financialization of the U.S. economy is following the same pattern as the financialization marked the beginning of the decline of Hapsburg Spain in the 16th century, the Dutch trading empire in the 18th century, and the British empire in the 19th century:

. . . the leading economic powers have followed an evolutionary progression: first, agriculture, fishing, and the like, next commerce and industry, and finally finance. Several historians have elaborated this point. Brooks Adams contended that "as societies consolidate, they pass through a profound intellectual change. Energy ceases to vent through the imagination and takes the form of capital."

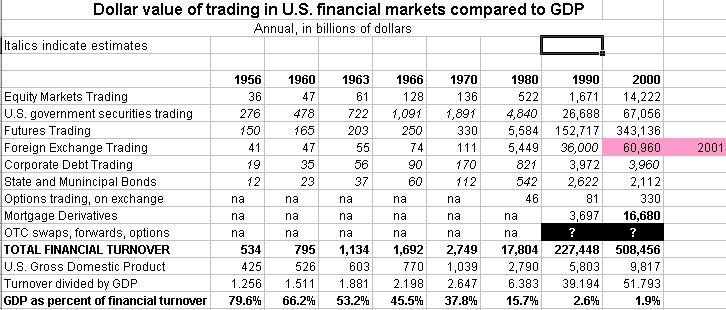

The roots of financialization can be traced to the rise of the radical free market doctrines of Milton Friedman and the "Chicago School of Economics," which provided the ideological and theoretical basis for the increasing deregulation of financial systems and banking beginning in the 1970s. One of the most important events was the end of the post-World War Two Bretton Woods system of fixed international exchange rates and the dollar peg to gold in August 1971. The demise of fixed exchange rates initiated a rapid rise in the level of foreign exchange trading (forex). In the United States, forex leaped from $110.8 billion in 1970, 10.7 percent of U.S. Gross Domestic Product, to $5.449 trillion in 1980, 195.3 percent of U.S. GDP.

Other financial markets exhibited similarly explosive growth. Trading in U.S. equity (stock) markets grew from $136.0 billion or 13.1 percent of U.S. GDP in 1970, to $1.671 trillion or 28.8 percent of U.S. GDP in 1990. In 2000, trading in U.S. equity markets was $14.222 trillion, or 144.9 percent of GDP.

According to the March 2007 Quarterly Report from the Bank for International Settlements:

Trading on the international derivatives exchanges slowed in the fourth quarter of 2006. Combined turnover of interest rate, currency and stock index derivatives fell by 7% to $431 trillion between October and December 2006.

(See page 24.) Thus, derivatives trading – mostly futures contracts on interest rates, foreign currencies, Treasury bonds, etc had reached a level of $1,200 trillion, $1.2 quadrillion, a year .

By comparison, U.S. GDP in 2006 was $12.456 trillion.

The table below provides data for the annual amount of financial trading in U.S. financial markets, compared to GDP.

Sources:

Equity Markets Trading, Statistical Abstract of the United States. For example 1990 and 2000 taken from Table 1201, Sales of Stocks on Registered Exchanges, 1990 to 2003, "Market Value of all Sales" minus "CBOE" Statistical Abstract of the United States, 2004-2005.

U.S. government securities trading, Statistical Abstract of the United States. For example 1990 and 2000 taken from Table 1190, Volume of Debt Markets by Type of Security, 1990 to 2003, Statistical Abstract of the United States 2004-2005.

Futures Trading, are estimates based on the average value of types of futures contracts, multiplied by the number of contracts traded, reported by the Futures Industries Association.

Corporate Debt Trading and State and Municipal Bonds, the Bond Market Association reports average daily volume, multiplied by 240 business days. http://www.sia.com/...

Options trading, on exchange, Statistical Abstract of the United States. For example 1990 and 2000 taken from Table 1201, Sales of Stocks on Registered Exchanges, 1990 to 2003, line for "CBOE" only, Statistical Abstract of the United States, 2004-2005.

Mortgage Derivatives, 2000 taken from Table 1190, Volume of Debt Markets by Type of Security, 1990 to 2003, Statistical Abstract of the United States 2004-2005.

OTC swaps, forwards, options is reported by the U.S. Federal Reserve Bank of New York, and the Bank for International Settlements, but I have not been able to determine what percentage of nominal values of these types of financial derivatives are actually traded.

In the Introduction to the 2006 book Financialization and the World Economy, editor Gerald A. Epstein wrote that

in the mid- to late 1970s or early 1980s, structural shifts of dramatic proportions took place in a number of countries that led to significant increases in financial transactions, real interest rates, the profitability of financial firms, and the shares of national income accruing to the holders of financial assets. This set of phenomena reflects the processes of financialization in the world economy . . .

finance benefits handsomely from the same processes that create economic crises and injure so many others. Hence the costs of financial crises are paid by the bulk of the population, while large benefits accrue to finance. Duménil and Lévy provide new and valuable data documenting these trends in the case of France and the USA . . .

Using the case of the US economy, Crotty argues that financialization has had a profound and largely negative impact on the operations of US nonfinancial corporations. This is partly reflected in the increasing incomes extracted by financial markets from these corporations; trends identified also by Duménil and Lévy and Epstein and Jayadev. For example, Crotty shows that the payments US NFCs paid out to financial markets more than doubled as a share of their cash flow between the 1960s and the 1970s, on one hand, and the 1980s and 1990s on the other . . .

Financial markets’ demands for more income and more rapidly growing stock prices occurred at the same time as stagnant economic growth and increased product market competition made it increasingly difficult to earn profits. Crotty calls this the ‘neoliberal’ paradox. Non-financial corporations responded to this pressure in three ways, none of them healthy for the average citizen: 1) they cut wages and benefits to workers; 2) they engaged in fraud and deception to increase apparent profits and 3) they moved into financial operations to increase profits. Hence, Crotty argues that financialization in conjunction with neoliberalism and globalization has had a significantly negative impact on the prospects for economic prosperity.

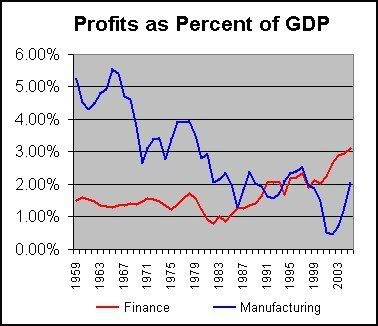

The graph below shows profits of the U.S. financial sector and of the U.S. manufacturing sector, as a percent of GDP

Source: Economic Report of the President: 2007 Report Spreadsheet Tables, Tables B-1 and B-91.

http://www.gpoaccess.gov/...

One of the most notable features of financialization has been the development of financial derivatives – financial instruments, the price or value of which is derived from the price or value of another, underlying financial instrument. The most common types of derivatives are futures contracts, swaps, and options. In the early 1990s, a number of central banks around the world began to survey the amount of derivative market activity, and report the results to the Bank for International Settlements.

In the past few years, the number and types of financial derivatives have grown enormously. In November 2007, commenting on the financial crisis sparked by the sub-prime mortgage collapse in the United States, Doug Noland’s CREDIT BUBBLE BULLETIN, on Asia Times Online, noted,

The scale of the Credit "insurance" problem is astounding. According to the Bank of International Settlements, the OTC market for Credit default swaps (CDS) jumped from $4.7 TN at the end of 2004 to $22.6 TN to end 2006. From the International Swaps and Derivatives Association we know that the total notional volume of credit derivatives jumped about 30% during the first half to $45.5 TN. And from the Comptroller of the Currency, total U.S. commercial bank Credit derivative positions ballooned from $492bn to begin 2003 to $11.8 TN as of this past June. . . .

A major unknown regarding derivatives is the actual amount of cash behind a transaction. A derivatives contract with a notional value of millions of dollars may actually only cost a few thousand dollars. For example, an interest rate swap might be based on exchanging the interest payments on $100 million in U.S. Treasury bonds at a fixed interest of 4.5 percent, for the floating interest rate of $100 million in credit card receivables. This contract would involve at least $4.5 million in interest payments, though the notional value may be reported as $100 million. However, the actual "cost" of the swap contract would be some small fraction of the minimal $4.5 million in interest payments. The difficulty of determining exactly how much this swap contract is worth when accounted for on a financial institution’s books, is typical of the worries many experts and regulators have over the explosive growth of these types of instruments.