The WSJ has a decent article describing the current financial crisis and pulling no punches:

Debt Reckoning: U.S. Receives a Margin Call

The U.S. is at the receiving end of a massive margin call: Across the economy, wary lenders are demanding that borrowers put up more collateral or sell assets to reduce debts.

The unfolding financial crisis -- one that began with bad bets on securities backed by subprime mortgages, then sparked a tightening of credit between big banks -- appears to be broadening further. For years, the U.S. economy has been borrowing from cash-rich lenders from Asia to the Middle East. American firms and households have enjoyed readily available credit at easy terms, even for risky bets. No longer.

The diagnosis is no longer, as still a few weeks ago, of a "softening" of the economy, with troubles limited only to arcane financial markets

Bob Eisenbeis, a former executive vice president of the Federal Reserve Bank of Atlanta, says the problem is more than an inability to find ready buyers for assets. "It is time to step back and recognize that the current situation isn't a liquidity issue and hasn't been for some time now," said Mr. Eisenbeis, the chief monetary economist for Cumberland Advisers. "Rather, there is uncertainty about the underlying quality of assets -- which is a solvency issue, driven by a breakdown in highly leveraged positions."

A crisis of liqudity means that you have assets, but cannot sell them in time to pay the debts you have. A crisis of solvency means that the assets you have are worth less than what you owe. It is often hard to tell which is which (is your asset illiquid because it takes time to sell, or because it is worth less than you are expecting to get for it?). A liquidity crisis can turn into a solvency crisis, if people are forced to liquidate assets in emergency fashion, and thus to drop prices to raise cash as quickly as possible - thereby creating market prices for these assets that are lower than before, and putting others that hold similar assets in the situation where their assets are suddenly worth less.

But we had an underlying solvency crisis from the start, given the unrealistic lending that had taken place - such as the "ninja" loans (no income, no jobs or assets) that were provided in the heat of the mania and which could only ever be repaid if house prices kept on going up. Asset prices were propped up only by the fact that people were able to borrow unreasonable amounts of money to bid for them, and were able to borrow such amounts only because they were seen to be acquiring valuable assets - ie the whole thing was a grand illusion, sustained by a collective loss of common sense, helped with massive dollops of self-interested propaganda by the financial, construction, real estate and media industries.

Now it's the same thing, in reverse. People cannot borrow, thus cannot bid for assets, whose prices fall down as they need to be sold - and those deep in debt need to sell (ar dump the assets to banks that then need to sell). As prices go down, all loans based on collateral dry out - and more generally banks are getting stingy as they struggle with all those doubtful assets on their hands, so lending dries out. This is what's called "deleveraging" in the case of the hedge funds, and it's as painful for financial assets as it is for real estate.

Kenneth Rogoff, a Harvard University economist, says the current difficulty has many mothers -- the housing bubble, the subprime problem and the fact that the value of U.S. imports has long outstripped the value of exports. The current account deficit -- the broadest measure of the trade deficit -- burgeoned, and the U.S. needed to borrow ever larger amounts of cash from abroad to fund it.

For years, Mr. Rogoff and like-minded economists harped that the U.S. current account deficit was unsustainable. But despite the belief that it would necessarily reverse, it kept growing through the first part of this decade, going from 3.6% of gross domestic product at the end of 1999 to a record 6.8% at the end of 2005. Lately, the deficit has seen a slight narrowing, but the combination of credit crisis and the economic downturn may have proved the catalyst for a faster, and potentially more dangerous, adjustment.

As in the first paragraph of the article, this is the closest this article, which correctly describes the current winding down, comes to the underlying cause, but it's simple: the country was living on foreign credit.

But I get the feeling that this is part of an attempt (likely to get louder as things get worse) to blame the "foreign" bit rather than the "credit" bit.

I hope I'm wrong, but as we begin to see loud calls for bailouts (unfair, as they reward the bankers that created the problem n the first place, but, you see, the alternative is worse), the availability of a ready-made outsider scapegoat is likely to be irresistible.

And yet, the fact remains that the problem is not who provided the credit, but the fact that it was provided in such large amounts.

Because that sea of debt had one real purpose: hide the fact that income for most are stagnating.

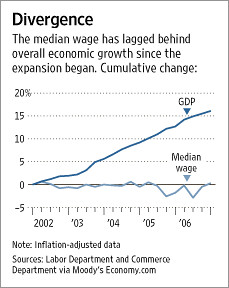

I never tire of posting this graph of the "W economy", because it summarises in a nutshell what happened: growth happened, but did not trickle down to the middle classes, let alone the poor. Thanks to wage stagnation, made possible by the threats of outsourcing and offshorisation, and by the demonisation, emasculation or dismantlement of regulations and institutions (like unions) protecting workers, the fruits of growth have been captured by a very few - and this has been hidden because consumption was propped up by readily available debt and the apparently growing virtual wealth of homeowners.

I never tire of posting this graph of the "W economy", because it summarises in a nutshell what happened: growth happened, but did not trickle down to the middle classes, let alone the poor. Thanks to wage stagnation, made possible by the threats of outsourcing and offshorisation, and by the demonisation, emasculation or dismantlement of regulations and institutions (like unions) protecting workers, the fruits of growth have been captured by a very few - and this has been hidden because consumption was propped up by readily available debt and the apparently growing virtual wealth of homeowners.

The problem is that, while a lot of that growth was illusory (and is now unravelling), the wealth capture that took place thanks to it was very real, and, in particular, the mechanisms ensuring that an ever grower share of the pie got into a few lucky hands are still in place, and will bite even more harshly as the pie shrinks.

In short:

The middle classes got a shrinking share of a growing pie, apparently staying somewhat ahead.

Now, they are about to get a shrinking share of a shrinking pie.

The current economic consensus - that of "labor market reform", of "unsustainable liabilities of Medicare", of "protectionism is the ultimate danger" - in short, of those that think that economic prosperity is correctly summarised by the value of the Dow Jones Index is the one that has been cheerleading the shrinking of the share of the pie (remember: labor market reform = lower wages. Full stop), and they are part of the problem, not part of the solution.

And you see that all the remedies are focusing on ways to make the pie be (or better, look) bigger than it can - more money injections, more cheap debt, more support for the financial sector.

They are the problem, not the solution.

Too much debt and not enough income was the problem.

And the solution is simple: stop debt (this is happening on its own anyway). and boost income.

How do you do that when there isn't enough money around?

By creating real activity rather than the money-shuffling kind.

And, as it were, there is a sector that is "real" and has an urgent need for action: infrastructure, and in particular energy-related infrastructure.

A plan that focuses on a few simple things:

- massive public support for energy efficiency refurbishment of existing homes;

- a massive, New Deal rural electrifaction scale plan to build renewable energy assets and the corresponding grid infrastructure;

- a similarly massive plan to develop smart public transportation, both locally and intercity;

Spending the money currently wasted in Iraq on these 3 things alone would provide a real boost to the economy in the sectors that actually need it, would reduce oil&gas consumption and carbon emissions, and be an actual investment in the future, as opposed to the current drain on the future that's been engineered via debt used on mindless consumption of junk.

Add in plans to boost minimum wage, reinforce union rights and tax imports of carbon-rich goods, and you'd have a pretty damn good economic - and geopolitical programme.

Because the problem is the most of America's population is living, by design, above its means. It is kept dependent, fearful and distracted while the happy few gorge. Call it what it is: class war. Time to fight back.