Last summer at Netroots Nation, Ezra Klein urgently advised everyone attending the health policy panel to pay close attention to Max Baucus. Ezra explained, all roads to healthcare reform lead through Max. He was correct.

If you want to know more about the man who holds the fate of healthcare reform in his hands, I urge you to read Ezra's excellent article about him, The Sleeper of the Senate, in the American Prospect.

Max Baucus is a key player and he happens to be in the thrall of the insurance lobby. They um, own him favor him.

He also happens to be the Chairman of the Senate Finance Committee.

His name is Max Baucus. He's a democrat from Montana, and I suggest you get to know this dude as well as AHIP knows and loves him.

Here's a link to Max's Open Secrets page, you decide where his heart resides.

If Max is anything, he's a wily politician. He talks about regulating the murderous insurance industry, but he doesn't say anything about what this regulation will look like. I trust common sense will prevail, and the plan will not be to have the insurance industry "regulated" by the same folks who regulated the criminals on Wall Street.

In an interview last week in the Wall Street Journal, Max waxed eloquent on the need for healthcare reform.

Here's some of what he said.

MAX BAUCUS:

I believe strongly that the opportunity is here for us in America to finally have a health-care system that we can really be proud of. But it’s got to be one where everybody is involved. Everybody: consumers, employers, providers, health-insurance companies, everybody. My judgment is that we’ve spent way too much time with patchwork, fixing this part here and that part there, push on the balloon, it bubbles up someplace else, and we just are getting nowhere and we have what we have — namely 40-some million people who don’t have health insurance, 25 million underinsured, a reimbursement system that is out of whack. It rewards volume, not quality. We also are not addressing costs, because costs are going up so much in our country. Costs to individuals, costs to businesses. And also the cost to the federal government with the Medicare trust fund going through the roof.

So my judgment is that first of all you have to have universal coverage. It’s a disgrace that the United States is the only industrialized country in the world without universal coverage. And the system cannot be repaired without universal coverage. I’m not saying single-payer system. I’m saying a uniquely American system which combines public and private coverage by expanding slightly Medicare, Medicaid, CHIP [Children’s Health Insurance Program], but also making sure that health insurance is available for everybody.

We have an employer-based system in our country. That’s the American system. Some suggest scrapping it. I don’t. I think we build on it.

We probably should go look at the employer-provided exclusion in the tax law because it’s regressive. It’s a little inefficient. But we also need to give incentives to small businesses and individuals so they get health insurance, too.

We need big incentives in changing the delivery system, and through Medicare rewarding quality, working through the National Quality Council, working with evidence-based outcomes, moving to again reward providers, hospitals and physicians based more on quality.

We all have to keep an open mind on all this stuff, figure out how to get to yes. Everything is on the table. The only thing that’s not on the table is a single-payer system. That’s going nowhere in this country.

Thus spoke Max Baucus.

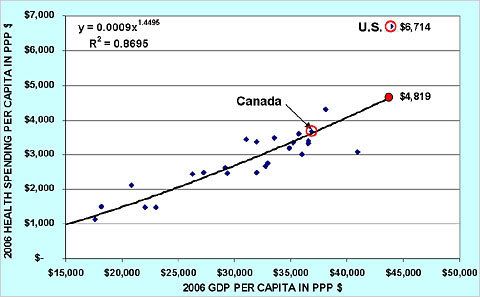

This is a snapshot of the system Mr. Baucus wants to save and rehabilitate.

Here you'll note what the United States spends per capita to provide healthcare to well under 100% of the population.

And in this beauty, note what the United States spends on healthcare compared to the other industrialized nations. And never forget we have 48 million with no access to healthcare

And one more. The shameful and depraved state of affairs across the United States.

But this is the system that Max and many other insurance industry bagmen and apologists will fight until death to defend.

Our so-called "leaders", in bed with the insurance industry, think they know how to fix the broken healthcare system. Central to the "fix" is maintaining the pre-eminence of the for-profit insurance industry.

Baucus, Kennedy, Wyden and Co. may throw a poorly funded public option into the mix to placate those of us (most Americans, no doubt) who are disgusted by the delay, deny and deceive Murder By Spreadsheet insurance industry. This public option could well become the underfunded repository of the chronically sick, those of us with pre-exisiting conditions the for-profits hate, and the usual motley crew of unloved and unwashed American who have the bad taste to get sick.

Are Baucus and Co. aware of the new report from the Commonwealth fund, which paints a bleak picture of the U.S. healthcare system?

There's some talk in the land about whether or not the United States can afford to move forward in a big way on bringing guaranteed and affordable healthcare to all Americans, a central campaign commitment of President-elect Obama.

Help can't wait. The news on the healthcare front is so bad, that the notion that we can continue to let Americans die because they cannot access healthcare is absurd.

The Domino Effect:

As these workers face the loss of their employer-provided health insurance, about 1 in 5 looks to COBRA (an acronym for the Consolidated Omnibus Budget Reconciliation Act of 1986) for help. Through COBRA, a laid-off worker can maintain the same insurance coverage he or she had through their previous employer, but at a cost. Specifically, they must pay the portion of their premiums that they had been responsible for, plus the portion that their employers previously paid -- as well as an extra 2 percent of this combined premium.

The increases are a bitter pill to swallow for someone who has just lost a job and likely has less money to spread around. And the small relief provided is only temporary. Those who cannot find another option within 18 months face a new scramble for coverage once this window expires.

"Unfortunately, the COBRA legislation guarantees laid-off workers the right to continue coverage at their own expense, but does not make that coverage affordable," said Dr. David Himmelstein, associate professor of medicine at Harvard Medical School and co-founder of Physicians for a National Health Program.

"Under COBRA, health insurers may charge higher premiums to sick individuals, so anyone with a chronic condition who really needs insurance will face astronomical premiums," he added. "As a result, the vast majority are likely to become uninsured quite quickly."

"The cost for coverage, coupled with no or substantially reduced [income], may force additional steps to secure cash flow, including mortgage leveraging, credit card and family borrowing, to the extent it is even available," said Jay Wolfson, associate vice president of Health Law, Policy and Safety at the University of South Florida. "And then, without new employment -- perhaps even before COBRA expires -- there is no reservoir for cash, and the cascade of additional economic difficulties may create a deadly flood."

Uwe Reinhardt, professor of economics and public affairs at Princeton University, has studied the U.S. health care system for the past two decades. He agreed that if the economic picture gets much worse, many families could be heading for disaster.

"If this recession gets any deeper and lasts several years, many Americans may lose whatever savings they have, should they or their family members get sick," Reinhardt said.

. . .The first domino falls when those who lose their jobs seek assistance through COBRA. If they can afford it, they will remain under their old policy and still pay premiums. But if they cannot, they will join the ranks of the uninsured.

For every person who becomes uninsured, health insurance companies lose revenue from monthly premiums. The situation worsens 18 months later, when those who opted for COBRA but have not yet been able to find a new employer-based plan, become ineligible for coverage. The insurance companies will take yet another hit.

"Insurance carriers, even the not-for-profit Blue Cross plans, are going to suffer mightily as layoffs accrue," Nash noted.

And this hit from lost revenue gets passed on to employers, who, in turn, pass it on to existing policyholders.

http://abcnews.go.com/...

There is no going forward as a nation, as American citizens are falling over a cliff. President-elect Obama knows this.

The health insurance industry lobby (AHIP)also knows this. They know the train has left the station. They're trying to stay on board in the worst way.

I'll leave you with this, The Ten Worst Insurance Companies in the United States; How They Raise Premiums, Deny Claims, and Refuse Insurance to Those Who Need It Most.

Wellpoint is number six on the list. Here's some light reading about this criminal enterprise which if Max has his way, is destined to become one of the crown jewels of the retooled U.S. healthcare system.

WellPoint has a long history of putting its bottom line ahead of the welfare of its policyholders and their health care providers. Investigations have shown that Wellpoint routinely cancels the policies of pregnant women and chronically ill patients.

. . .California is making an aggressive effort to force

WellPoint to stop engaging in practices it believes are illegal.

In March 2007, the state’s Department of Managed Health Care fined Blue Cross of California and its parent company,WellPoint, $1 million after an investigation revealed that the insurer routinely canceled individual health policies of pregnant women and chronically ill patients. The practice, known as rescission, is illegal in California.

. . .Other states have taken action against WellPoint and its

subsidiaries over their claims-processing practices. In January 2008, Nevada Insurance Commissioner Alice A. Molasky-Arman announced a $1 million settlement with Anthem Blue Cross and Blue Shield over systematic overcharging of policyholders. Similarly, Colorado’s Insurance Commissioner, Marcy Morrison, secured a $5.7 million refund for consumers of Anthem Blue Cross Blue Shield health insurance policies.109 In Kentucky, the Office of Insurance ordered Anthem Health Plans of Kentucky

to refund $23.7 million to 81,000 seniors and disabled people over inaccurate Medicare claims payments.

http://www.justice.org/...

Wellpoint is one of the companies Max Baucus wants to leave as the custodian of your health and mine.