We didn't break Fannie Mae and Freddie Mac, but we own them. Taxpayers have already paid $112 billion to the two entities. Now we may be doubling-down on that bet. According to the New York Times, shortly before Christmas the Obama administration,

"quietly disclosed that it had, in effect, given the companies a blank check by making their federal credit line unlimited; the ceiling had been $400 billion."

But, what are we getting for our billion dollar investment?

Wall Street, K Street, and our leaders in Washington tell us that helping Fannie Mae and Freddie Mac is essential to helping the US housing market recover. But, it doesn't appear that Fannie Mae or Freddie Mac are necessarily committed to that goal. They are, instead, pretending like it is still 2005 and housing prices will never fall.

Rather than forgive some of the principal balance of homeowners who are facing foreclosure, Fannie Mae and Freddie Mac both expressly prohibit their mortgage loan servicers from lifting some of the burden from underwater homeowners.

First, a little background, Fannie Mae and Freddie Mac are both Government Sponsored Enterprises otherwise referred to as a "GSE." A government-sponsored enterprise is a shareholder-owned company created by Congress to serve a public purpose. Fannie Mae was created as a government agency by President Franklin Roosevelt in 1938 to stabilize and provide mortgage loans during the Great Depression. In 1970, Freddie Mac was created to compete with Fannie Mae.

Neither directly originate mortgage loans, but they do agree to purchase the loans originated by others. Thus, they provide immediate payments to lenders for originating the loans and lowering the risk to those lenders if loans default. Often the mortgage servicing rights are retained by the original lender or Fannie Mae/Freddie Mac hire a new mortgage servicer. So, although you may pay CitiMortgage or Chase every month, the loan may actually be owned by Fannie Mae and Freddie Mac (which means that the loan is actually now owned by us---the taxpayers).

Each of these mortgage servicers are required to follow and adhere to Fannie Mae and Freddie Mac's servicer guides. The servicers cannot do anything that is not allowed by the servicer guide. And, do you know what is expressly not allowed in the servicer guide? That's right---principal reduction.

Even if a home has lost $100,000 in value and it makes no financial sense to proceed with foreclosure, Fannie Mae and Freddie Mac prohibit their servicers from reducing the principal balance to get an affordable payment. For example, page 11 of Fannie Mae's HAMP Guidelines expressly state:

"A principal write-down or principal forgiveness is prohibited on Fannie Mae mortgage loans."

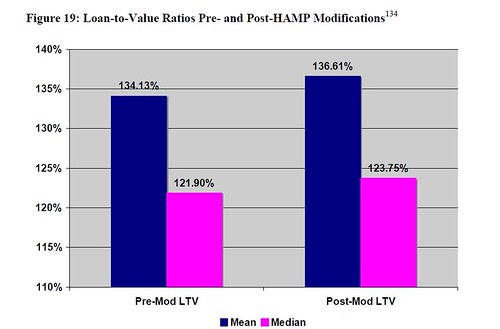

How this plays out in real life was revealed in Professor Elizabeth Warren's October Report related to HAMP. In that report, she found that although monthly payments were reduced the loan-to-value ratio for post-mod HAMP loans was worse than the non-modified loans. The ratio was a shocking 136%, meaning that people owed 36% more than their home is worth. See page 54 of the report.

Of course, Congress could fix all of this by allowing cram-down or judicial modification of mortgages through bankruptcy. But, at the very least, Congress has to order Fannie Mae and Freddie Mac to lift the ban on reducing the principal balance of mortgage loans. Again, we own these companies, and ending zombie homeownership is the key to getting our overall economy back on track.

About 20 to 30% of homeowners are underwater, we aren't doing anybody any favors by allowing Fannie Mae and Freddie Mac to push homeowners even further underwater with HAMP loan modifications that don't reduce the principal balance of mortgage loans.