If you’re like me, you’re appalled by the influence of the financial industry in every aspect of public life, from spending on elections to the recent decision of Visa and Mastercard to stop processing donations to Wikileaks. I think I speak for a lot of people on this site and in America when I say that I’ve lost trust in the financial system.

Frank Rich:

Many of America’s best young minds now invent derivatives, not Disneylands, because that’s where the action has been, and still is, two years after the crash.

Part of the genius in setting up this site was to harness the power of the internet in the form of crowdsourced contributions, and this site became a community more than a news organization. (And I'm really excited about Kos' vision for DK4.) DailyKos is part of the movement that has changed the nature of journalism in the past 10 years by forcing accountability on the fourth estate.

I believe that something similar may be happening with the financial industry.

Let me explain: I may be representative of the "dumb money" (as stated in gjohnsit's Global Banks Beginning to Fear Unruly Peasants) that is invested in Wall Street. I have a small 401k, but I really don’t care to learn what all of these terms mean and why the market goes up and down on a daily basis. It all seems silly to me and I have better things to do with my time than obsess about arbitrary financial movements.

However, the problem is that safe, steady investments like a savings account generally only earn a pittance of interest, so you might as well roll the dice on the market, right?

Peer to Peer Lending

P2P Lending is the process of making microloans ($25-50) to a number of people and collecting the interest. Since you can only lose a small amount to each person defaulting, then you spread your risk out among a number of people and end up with a pretty solid investment. Weighing the risk vs. the reward it still comes out a lot better than most investments (like that dinky 1% you get on a savings account or CDs).

I don’t want to rewrite the many sources describing P2P Lending, so if you want an introduction to peer to peer lending, check out this diary by Rmonroe in January 2009.

Or on the NY Times:

The math pitch involves the increased efficiency of cutting out the banks, allowing relatively lower rates for borrowers and good returns for lenders. (emphasis added)

Or the WSJ:

"It just felt like it was doing nothing. It was as good as putting it under my mattress," says Ms. Stitzel, who works for a medical-device company in Seattle and has seen her investment grow by about 13% since February. "I'm not a philanthropist. This is an investment for me." (emphasis added)

But basically, it's like an online credit union, where people will borrow from YOU instead of financial institutions. Another analogy: it's kind of like Kiva, but for profit. Even if Ms. Stitzel isn't a philathropist, you can be.

The two biggest P2P lending sites are Lending Club and Prosper. (I won't link - this isn't an advertisement.) I've opened an account on Lending Club, but not Prosper.

A Political Investment?

Bear with me, I'm going to spell out how this can be a political investment. It's a place to invest your money for which the vast majority of the proceeds accumulate directly to you, and not to intermediaries. I believe that P2P Lending can be a direct heir to the "Move Your Money" movement that sought to move money out of major banks. And if you can defund major banks, then you reduce their political influence, political ad-buying, and generally pernicious, self-serving behavior.

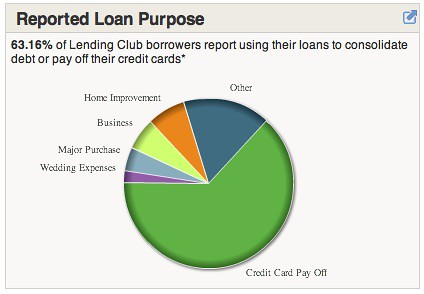

And, well, there's also another way that this is potentially hurting the banks. Check out this screenshot from Lending Club:

Over 60% of the loans given are stated to be for consolidating credit card loans. So let me be clear about this: that 10-20% (or whatever) interest that banks are charging for credit card balances.... could be coming to you instead. And people are happy to pay that interest to you, because they can often get a lower interest rate than their credit cards.

There is risk, but if you spread your money out on a number of loans then you can minimize your risk. Lending Club reports that 82% of investors with 100+ notes earn returns between 6% and 18%. It's not perfect, and you can expect some defaults, but those are pretty good odds to me! Compare it to the interest rates you get on a CD and you'll see why it might be a good idea.

Investing in People, Not Corporations

What does this mean? By investing in P2P lending, you're investing in people, not corporations! P2P Lending also directly deprives credit card companies their revenue streams from the ridiculous interest rates they charge on their cards, and puts that money in your pocket.

You might also be thinking – well, who says these websites are any more responsible than the TBTF banks? Well, they might not be, but in effect these websites are go-betweens and not financial entities. They take a small percent of each transaction, but the bulk of the interest and money transacted through the site flows directly back to the lenders (i.e. you). I can’t say with any confidence that these websites would be good corporate citizens – I just have no idea – but they won’t have the advantages that traditional banks do of keeping all that money.

Think of it as a revolutionary way that uses the power of the internet to subvert the banks’ hold on our financial system.

This Is Not An Advertisement

This diary isn’t meant as a commercial for these sites, and if you’re considering an investment please think about it very carefully.

I know that with all of the discussion on this site about the jobs crisis, a diary about investment may seem to be poorly timed. Well, I'm no fat cat; I have a small account (less than $600) that I’ve been feeding slowly over the last year with spare change. My plan is to keep feeding the account and create an income stream that I can tap if I go back to grad school. At that point, even an extra couple bucks a month would go a long way. And since I'm paying 7.14% interest on my existing student loans, this seems to be one of the few ways I can actually come out ahead if I want to invest money instead of just paying off loans. All of this is why I don't mind parking some money and not touching it for 3-5 years.

I haven’t had any of the people I've lend to default on their loan yet, so my experience has been completely positive. Make of that what you will, but I feel obligated to offer a few insights into how these accounts work and if they might be worthwhile to invest in:

ADVANTAGES:

-Terrific interest rate for you, and they don’t charge very much in fees

-Can create steady monthly income stream

-Removes money from financial industry, puts it in your pocket

DISADVANTAGES:

-Very illiquid, most loans are for 3 to 5 years. Once your money is in, it’s really tough to get out. (Consider this carefully.)

-Can be risky, especially if you lend to people with lower credit scores (at higher interest rates.)

-It’s kind of slow. It makes sense, but each little transaction takes like a week to process.

The Last Word

I want to see change come to America, and I believe that there are ways to bring that change that don't involve overtly political acts like supporting a candidate, canvassing, phone banking etc. Those are still really important, but you can support change every single day of the year with things like your investments.

So I throw this out there with a sense of humility. This is the type of community that can get behind an idea for the right reasons, and there has not been an in-depth diary on P2P Lending as far as I know. So it's an exciting idea that I felt was important for this community to be aware of, and potentially pursue if it makes sense on an individual basis.