A quick look at who wins and who loses if Eurozone Sovereign were consolidated and paid collectively.

Yglesias advocates for Eurobonds as a solution to Greece's sovereign debt problems,

It would start with the recognition that Greece is insolvent. It can’t pay the money it owes. One or two or maybe three other countries also may be insolvent. And the existence of solvency problems in some states is creating liquidity problems for other larger states. So there’s some insolvency, and even though the insolvency is concentrated in a relatively small number of small states it’s a problem for a much broader set of European people. At the same time, if you look at the total amount of sovereign debt in Europe and compare it to the Eurozone’s total fiscal capacity, the debt is very manageable. The Eurozone as a whole is a very solvent, creditworthy entity. So in principle you could consolidate all that outstanding European debt into a single Eurozone-wide debt financed by a modest European Solidarity VAT Surcharge.

Let's drill down a bit:

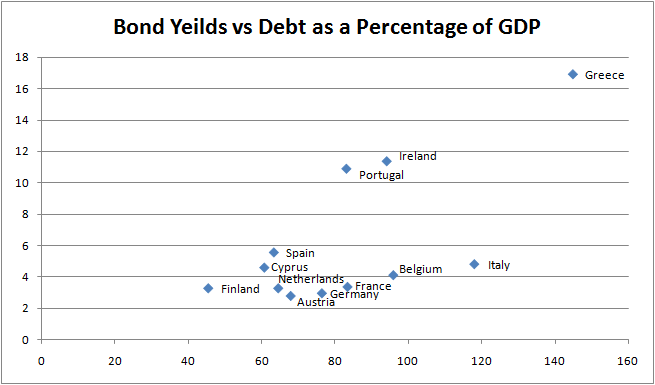

Ten-year bond yields plotted vs Public Debt as a Percentage of GDP. Some countries do not have liquid 10-year note markets, and so have been excluded from the chart. See ECB estimates.

The bond markets seem to be treating Ireland, Portugal, and Greece differently than most countries relative to their debt burden. One potential explanation is that the Euro is crushing their growth expectations and making them permanently unable to pay their debt, another is that those countries are caught in some sort of cycle of bond-market irrationality and interest payment forced austerity. I don't know enough about economics to say which it is, but growth expectations in Italy and Ireland seem to be similar.

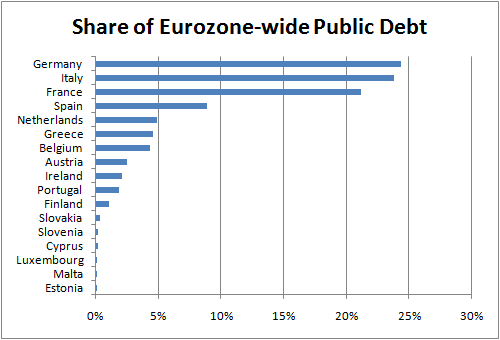

Total Eurozone Public debt is 84% of Eurozone GDP, while France's Public debt is 83.5% of GDP. So assuming that Eurozone-wide bonds would pay the same rates, a Yglesias-style consolidation of Eurozone Sovereign debt would save about 131 billion dollars a year in debt servicing costs, or about 1% of GDP.

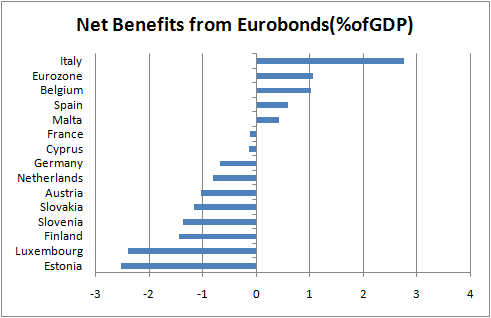

Net benefit from an assumption of national debt by a Eurozone-wide authority as a percentage of national GDP. This is assuming all debt is held in 10 year notes, which is very inaccurate, but still useful for the purposes of the post.

Same graph as earlier, with Greece, Ireland, and Portugal excluded for clarity. Eastern Europe comes out as the largest loser due to their very low debt burdens (Estonia's public debt just over 9% of GDP).

This is all relative to the status-quo, which looks unsustainable. Relative to Greek default, the net benefits for Germany are probably much better...