A version of this story is published at The People's View.

To say that there is panic in much of this side of the blogosphere about a meme that President Obama is trying to "cut" Medicare and Social Security would be an understatement. The fever pitch of those who seem to think Paul Ryan is a better friend of Medicare than President Obama has reached a high level.

The panic-mongering, as usual, has no basis in reality. We should at the outset remember some things President Obama has already done as part of health reform to increase benefits for those on Medicare:

- Collapsed, eventually completely closing the Part D prescription drug donut hole.

- While the donut hole is being shrunk over time, seniors in that gap get a 50% discount.

- Medicare (Part B) recipients now have free preventive care, eliminating copays for them under the old system.

The President

has said that he is willing to do entitlement reform, Medicare reform specifically, to strengthen the program and ensure its financial viability. Let's look at what such an approach might look like.

In his press conference on July 15, the President alluded to just what sort of reforms he might be looking at:

And so what we’ve said is a lot of the components of Bowles-Simpson we are willing to embrace -- for example, the domestic spending cuts that they recommend we’ve basically taken.

Oh noes! The dreaded Catfood Cumishun

TM! Everyone start screaming and yelling uncontrollably! Well, I am sure I am the naive one here - and President Obama, and if not me, definitely him - but I think it's worth looking at the

Fiscal Commission's final report and actually analyze their recommendations on Medicare and compare it with the current system. In it are cuts to provider payments, as well as payments to drug companies. But unless we are sadface about the plight of the drug companies and the hospital industry, I have to assume that these "concerns" revolve around the following parts:

3.3.2 Reform Medicare cost-sharing rules.

(Saves $10 billion in 2015, $110 billion through 2020)

Currently, Medicare beneficiaries must navigate a hodge-podge of premiums, deductibles, and copays that offer neither spending predictability nor protection from catastrophic financial risk. Because cost-sharing for most medical services is low, the benefit structure encourages over-utilization of health care. In place of the current structure, the Commission recommends establishing a single combined annual deductible of $550 for Part A (hospital) and Part B (medical care), along with 20 percent uniform coinsurance on health spending above the deductible. We would also provide catastrophic protection for seniors by reducing the coinsurance rate to 5 percent after costs exceed $5,500 and capping total cost sharing at $7,500.

3.3.3 Restrict first-dollar coverage in Medicare supplemental insurance.

(Medigap savings included in previous option. Additional savings total $4 billion in 2015, $38 billion through 2020.)

The ability of Medicare cost-sharing to control costs – either under current law or as proposed above – is limited by the purchase of supplemental private insurance plans (Medigap plans) that piggyback on Medicare. Medigap plans cover much of the cost-sharing that could otherwise constrain over-utilization of care and reduce overall spending. This option would prohibit Medigap plans from covering the first $500 of an enrollee’s cost-sharing liabilities and limit coverage to 50 percent of the next $5,000 in Medicare cost-sharing. We also recommend similar treatment of TRICARE for Life, the Medigap policy for military retirees, which would save money both for that program and for Medicare, as well as similar treatment for federal retirees and for private employer-covered retirees.

Look bad? Okay, let's tackle these one by one. First, cost sharing, the concept of a universal deductible and so forth. As anyone who is on Medicare knows, it already has a system of premiums, copays, and so forth, which should take away the pretense that any cost sharing at all is a "benefit cut" in Medicare. First of all, in the current Medicare system, there is no limit to one's out-of-pocket expenses. Let's see how Medicare works right now and how it compares and contrasts with what is being proposed by the Commission report.

Here is how the Medicare Part A and B cost sharing currently works. One might even say it's a rather regressive system. Let's look at the cost sharing in Parts A and B under the current system.

Part A: (pays for inpatient hospital, skilled nursing facility, and some home health care) For each benefit period Medicare pays all covered costs except the Medicare Part A deductible (2011 = $1,132) during the first 60 days and coinsurance amounts for hospital stays that last beyond 60 days and no more than 150 days.

For each benefit period you pay

A total of $1,132 for a hospital stay of 1-60 days.

$283 per day for days 61-90 of a hospital stay.

$566 per day for days 91-150 of a hospital stay (Lifetime Reserve Days).

All costs for each day beyond 150 days

Skilled Nursing Facility Coinsurance

$141.50 per day for days 21 through 100 each benefit period.

Part B: (covers Medicare eligible physician services, outpatient hospital services, certain home health services, durable medical equipment)

$162.00 per year. (Note: You pay 20% of the Medicare-approved amount for services after you meet the $162.00 deductible.)

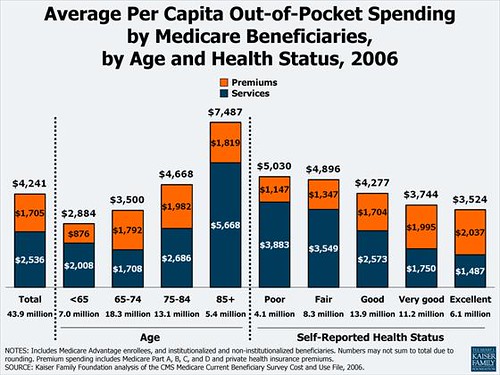

So what kind of cost sharing do people on Medicare currently actually go through? The average out-of-pocket expense (adjusted for inflation from 2006 numbers) is just under $5,000, and the older you are, the more your OOP expense grows. The Kaiser Family Foundation has a chart to demonstrate:

The distribution is obviously slanted more towards sicker people who pay a lot more in out of pocket expenses - 5% of Medicare recipients pay more than $5,000 a year in out-of-pocket costs account for 35% of total cost-sharing liability under Medicare (data from CMS). As you can see from the above chart, older seniors - who are also at the greatest risk of running out of their savings - have a much higher average out-of-pocket expenses. Because those with the highest costs are probably also the most struggling with their costs, a catastrophic cap ($7,500) should actually help those most in need.

All in all, for the vast majority of people, in terms of benefits, these changes won't make that much of a difference. It is difficult to say exactly for whom the out-of-pocket expenses will increase or decrease, of course, since it will depend on the individual, their health conditions and habits, and the services they use.

Medigap reform: Now, let's come to the changes proposed in the Medigap plans. Often called Medicare Supplement insurance, these plans cover expenses that Medicare won't, and/or only partially cover. What the Commission report is talking about is eliminating first dollar coverage - prohibiting Medigap plans from covering the first $500 and any more than 50% of the next $5,000 in Medicare cost-sharing. The rationale is that that coverage encourages overuse of medical services. It's important to remember that when we are talking about over-utilization, for the most part, we are not talking about "greedy" seniors who see their doctor "too much." No, we're talking about test-happy doctors and institutions, and for-profit device manufacturers fraudulently pushing "power-chairs" to people who do not need them, and overcharging for people who do. This is something I don't think most people having a cow every time someone talks about over-utilization understand.

But even if one does not accept that argument - or is ideologically duty-bound not to accept that argument - here is one thing about Medigap: The average Medigap plan costs $2,329 in premiums per year, making sure only relatively well-off seniors can buy them. If anything, this reform saves costs on the end of physicians and medical facilities that who will be more careful about procedures and equipment to order, which might even improve, rather than degrade, quality of care by focusing on health and wellness and care and not as many procedures and equipment as can be paid for.

In fact, A KFF study (which I will cover in detail later in another post) finds that even with these reforms, seniors on Medigap would pay less in Medigap premiums and cost-sharing than under the current system.

As we discuss the future of Medicare, we also need to remember a critical reality: According to the latest Trustee report, Medicare's trust fund starts running a deficit in 2024. Without any reform, every single current Medicare recipient who plans on living at least another 13 years will get an automatic and immediate cut in benefits.

So... yeah. I think everyone should calm down, study the issue, learn something before they start going fever pitch. The reforms being proposed, along with the Affordable Care Act and further reforms in prescription drug and provider payment schedules, are actually substantive ideas that preserves and strengthens Medicare, and our health care system as a whole.