Here’s my response (below) to the following posting that appeared on my Facebook timeline yesterday.

FYI- very close friend friend and son with bcbs got notice hospital insurance as of jan 1st goes from $420 to $845 for silver plan with a 5000 deductible. There is a bronz, silver, gold and platinum. Cant imagine what gold or plat. would cost. WHERE IS OBAMAS $2500. MAX YEARLY COST???????????? THATS EITHER A MAJOR LIE OR STUPIDITY . POSSIBLE REDUCTION WITH SUBSIDIES BUT YET TO BE DETERMINED. YOU CAN BE SURE IT WONT COME CLOSE TO WHAT IT WAS MUCH LESS THE STATED 2500.00.

1) The Affordable Care Act(ACA aka Obamacare) was created to offer health insurance plans and (expanded) Medicaid for the 40 million of our fellow citizens that either could not afford and/or were not eligible for health insurance.

It does not affect folks that currently receive health insurance through their employer. Everyone can agree that the initial rollout of ACA was an unmitigated disaster and the good news is that the website continues to improve; Visitors can now shop for competitive plans without having to provide personal data by clicking this link:

http://kff.org/...

Please share this link with your friend so he/she can determine their “possible reduction with subsidies.” And ask about the cost after subsidies for the lower cost Bronze Plan.

2) The ACA offers more comprehensive coverage and protections on the individual market. The Kaiser Foundation summarizes the increased coverage here:

http://kff.org/...

Under Obamacare, health plans must cover doctor visits, hospitalization, prescription drugs and maternity care without restrictions for pre-existing conditions, or physical or mental illnesses or conditions that existed before coverage began. These plans are generally more comprehensive than those on the individual market now and must cover any pre-existing conditions. They cover preventive services like immunizations, screenings and contraception at no expense to you. All plans must cover maternity care and childbirth without any extra coverage costs. You can no longer be required to give your detailed health or medical history to apply for coverage.

Not to minimize the “sticker shock” of your friend, but perhaps he/she will have reduced out of pocket costs to factor into overall healthcare costs going forward.

And there are new protections in the new marketplace. The ACA allows your friend’s son to remain on the family plan to age 26 and prohibits insurance companies from charging more or dropping individuals from plans due to a chronic health conditions. Here’s a link that spells it out pretty well.

https://www.healthcare.gov/...

It is totally understandable that folks that currently have individual health insurance policies (like Blue Cross Blue Shield) are finding out that their policies are being discontinued and are being forced to shop on the healthcare exchange. Here’s a recent article in the Charlotte Observer focusing on that circumstance. http://www.charlotteobserver.com/... Read this articleand continue to read this diatribe (below) for more analysis.

3.) Debunking the $2500 myth. Here’s a link that drills down into what President Obama said and when he said it as well as a source that debunks other false claims (Obamascare?) by Senator Cruz:

http://www.factcheck.org/...

Here’s the quote from President Obama made before the ACA became law:

Obama, May 13, 2009: On Monday I met with representatives of the insurance and the drug companies, doctors and hospitals, and labor unions, groups that included some of the strongest critics of past comprehensive reform proposals. We discussed how they’re pledging to do their part to reduce our nation’s health care spending by 1.5 percent per year. Coupled with comprehensive reform, this could result in our nation saving over $2 trillion over the next 10 years, and that could save families $2,500 in the coming years — $2,500 per family.

Perhaps the $2500 claim is not based entirely on facts?

4.) Not everybody is upset about the opportunity to purchase affordable health insurance. Here’s a video (I made) from the dark days before the ACA was enacted:

Procuring health insurance is a life or death matter for many.

Folks enrolling in Obamacare are tweeting about their experiences here: https://twitter.com/...

5.) Why Obamacare sucks in North Carolina. More than 1.5 million NC citizens do not have health insurance. That equals the population of Charlotte, Raleigh, Greensboro, Asheville, and Wilmington combined. More than 10,000 NC families declare bankruptcy each year due to medical emergencies. Our nation had to address the broken healthcare system and we came up with the crappy ACA. And our North Carolina legislature decided to make it worse. Consider the following facts:

Our elected leaders rejected expanding Medicaid for 500,000 of our low income neighbors. The expansion of Medicaid is an integral part of the ACA and would have brought billions of dollars into our state. To quote from a Raleigh News and Observer article:

Expanding Medicaid would have given more patients access to routine doctor visits, medicines and hospital care so they wouldn’t have to wait until problems develop into emergencies.

“We want people to have access to good, regular health care to help them stay healthy instead of having to treat them at the last minute,” said Bob Seehausen, senior vice president of Novant Health in Winston-Salem.

Expanding Medicaid in North Carolina could have helped our hospitals. Medicaid reimburses hospitals for treating patients unable to pay their medical bills. That’s an

estimated $660 million not flowing into our hospitals- each year (see link above). And we are treated to headlines like this one: “

North Carolina Hospital Closes Citing No Medicaid Expansion”

Of all the decisions made by our elected officials, deciding not to expand Medicaid on behalf of our citizens is the worst. Hundreds of thousands of people in North Carolina will make too much money to qualify for the existing Medicaid program and make too little money to afford to get on the healthcare exchange. Here’s a link and a statement from the ACA website:

When the health care law was passed, it required states to provide Medicaid coverage for adults between ages 18 and 65 with incomes up to 133% of the federal poverty level, regardless of their age, family status, or health.

It also provides tax credits for people with incomes between 100% and 400% of the federal poverty level to buy private insurance plans in the Marketplace.

Under the law, the federal government will pay states all of the costs for newly eligible people for the first three years. It will pay no less than 90% of the costs in the future.

The U.S. Supreme Court later ruled that the Medicaid expansion is voluntary with states. As a result, some states are not expanding their Medicaid programs as of January 1, 2014.

Many adults in those states with incomes below 100% of the federal poverty level fall into a gap. Their incomes are too high to get Medicaid under their state’s current rules. But their incomes are too low to qualify for help buying coverage in the Marketplace.

Nationwide estimate for adults falling into this “gap” is 5.2 million people according to a recent study by the Kaiser Family Foundation.

If you are an individual (on your own) in North Carolina making less than $11,500 per year, you cannot purchase insurance on the healthcare exchange. And qualify for Medicaid without the expansion through ACA? Here’s a handy chart (pdf.) depicting Medicaid (and CHIP) eligibility requirements for each state.

So your friend is upset about his premium going up (not counting the subsidies offered) but imagine how angry he/she would be if and when the existing policy is no longer offered and health insurance becomes unattainable. That is happening because the ACA was designed to expand Medicaid to fill the gap! Medicaid expansion would have (should have) been available for individuals making up to $15,405 per year - but our North Carolina government leaders rejected this assistance.

Now some may contend that our state cannot (or could maybe not) afford to begin to pay the 10% of the new cost after three years of the Medicaid expansion. But the State could opt out after three years and incur no additional cost. So really, what is there to lose by providing healthcare benefits to our low income working citizens for three years? (only askin’)

Another reason Obamacare sucks in North Carolina is the ill fated decision by our elected leaders to not set up a statewide exchange. We have a healthcare exchange - it’s the federal healthcare exchange. And there’s a charge for that. To wit: “the federally facilitated exchanges will be funded through monthly user fees paid by participating insurance issuers” This means that the private insurance companies pay the federal government a projected 3.5% premium on each and every policy and guess who that gets passed on to?

But the real rub is that because we did not expand Medicaid and did not set up a statewide healthcare insurance exchange. Only two insurers have offered to compete in our state. There’s a reason that premiums are higher in North Carolina and the reason is because there’s less competition. Specifically, Blue Cross Blue Shield is the only provider in 61 of our 100 counties (Coventry joins in 39 counties). No statewide exchange = Less Competition = Higher Premiums. Read this article from Raleigh News and Observer.

Kentucky cooperated with the ACA and expanded Medicaid and set up their own exchange and guess what? They have five insurance companies competing for business. It seems that more insurers are interested in Kentucky because they do not have to include lower income people (who tend to have poorer health and health outcomes) in their pool. Your friend’s Obamacare policy would cost a lot less if he lived in Kentucky.

Here’s a link to the Kentucky Health Exchange: https://kyenroll.ky.gov/

The only silver lining for the North Carolina version of Obamacare is that it can be improved. North Carolina can follow Kentucky’s path of setting up our own healthcare exchange by Executive Order (Governor’s Office). We can reverse course and expand Medicaid using the funds already authorized and available. Besides improving the health and well being of our citizens, we would attract more competition and lower the costs of your friend’s premium. States like Virginia and Ohio and more in Ohio and New Hampshire and Indiana, Pennsylvania, and Tennessee that have resisted implementing the ACA are now revisiting their positions.

6.) Obamacare sucks and we deserve better. One reason that Obamacare polls so poorly is that many people do not like to have to deal with private health insurers at all. It’s fine and good that more people will now have access to health insurance and healthcare, but it could be so much better. A bill was introduced in U.S. House of Representatives (H.R. 676) in 2009 titled “The United States National Health Care Act” that would have put an end to the monopoly held by private insurance companies. The act wouldn’t end the industry as citizens would have the right to purchase supplemental insurance. The purpose of the act would be to expand Medicare services to all Americans. It’s also called “Universal Health Care.”

Wiki link here.

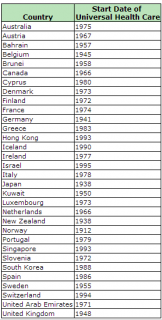

Healthcare is a right in our country as enumerated in our Constitution. (as in we have the right of “Life, Liberty, and the Pursuit of Happiness“) This is not a new concept. Consider the following graph:

Lots of developed countries provide universal health care for its citizens.

7.) We deserve better than Obamacare (imo) and we certainly deserve better than the Obamacare we have in North Carolina. It’s unfortunate that your friend is experiencing sticker shock in examining the NC Healthcare Exchange. There are things we can do (right now) to improve the system in our state. Can we agree that more education (research, examination, advocacy, etc.) is needed in our search of a better healthcare system for the future? Can we agree that our elected leaders in North Carolina should join other states and reconsider how best to implement the ACA to better suit our needs? (Say yes!)