Money markets signal fears over banks

Money markets in the US and Europe are signalling renewed fears about the financial strength of banks, with key confidence barometers almost returning to the levels that preceded the collapse of Bear Stearns.

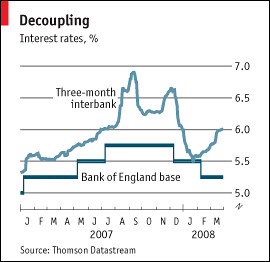

The concerns are being highlighted by the difference between overnight lending rates set by central banks and three-month Libor, the rate at which banks lend to each other. This spread, known as the overnight index swap rate, has been rising in the US and remains elevated in Europe, indicating that banks are reluctant to lend to each other.

This means that mortgage rates are going up even as central bank rates are going down, and it means that banks still see more skeletons in each other's accounts. More scrificial lambs mght be needed...

And the result?

IMF puts cost of credit crisis at $945bn

The financial sector faces potential losses of almost $1,000bn as a result of the credit crisis, the International Monetary Fund said on Tuesday, warning of further losses and writedowns on prime mortgages, commercial real estate, leveraged loans and consumer finance.

The IMF said total losses and writedowns would reach about $945bn, based on market prices in mid-March. Banks would suffer slightly more than half the total losses, with the rest falling on insurance companies, pension funds, hedge funds and other investors.

A trillion dollars? Hey, it's less than the war in Iraq! Maybe we can call that a "Greenspan" (or a "Bush"?)

But even before the next round of panic strikes, one might want to remember a simple point: deregulation and "reform" have been promoted endlessly as a way for companies to more more competitive, generate more profits (which would provide the investment of tomorrow and the jobs to follow). The main arbiter of whether any entreprise was successful was the valuation of these profits, and expectations of the same into the future, through stock prices. In that context, lower wages were a good thing, multi-hundred million pay outs to hedge fund managers a sign of dynamism, and only suckers did not go deep into debt.

Banks, hedge funds and investors have become the sole legitimate arbiters of "worth" under that system - and they have now proven beyond any doubt that they are profoundly unable to manage, let alone understand, such worth (taken away from ordinary workers), given that they have lost huge chunks of it.

Now that we have a $1 trillion proof of the profoundly mistaken faith in financial capitalism, can we please stop listening to financial analysts, economists and other self-interested rideralongs when discussing prosperity, success and what supposedly needs to be done to improve the lives of citizens?

Deregulation and "reform" does not work. Looting the workers does not create prosperity, it only helps transfer it from one sector of the economy (which creates it) to another (which wastes a good chunk of it, but given how few people share the spoils, it's still worth it for them, obviously).

How much more proof do we need? Another panic, as almost ironically predicted by the same financial analysts and market players?

Or will banks' own admission of their profound flaws suffice?

Banks take blame for credit crisis

The world’s leading banks on Wednesday publicly accepted much of the blame for the credit crisis in an attempt to stave off calls for more regulation, even as the International Monetary Fund slashed its estimates for global growth and warned that the US would suffer a recession.

The Institute of International Finance, representing more than 375 of the world’s largest financial companies, acknowledged “major points of weaknesses in business practices”, including bankers’ pay and the management of risk.

(...)

The IIF report detailed banks’ failings in managing risks, conflicts of interest over bankers’ pay, over-reliance on models, and inadequate protection against liquidity shortages. It also pointed to failures in credit ratings agencies and the dangers of mark-to-market accounting at times of illiquidity in creating a vicious circle of forced asset sales, lower prices, further writedowns and more asset sales.

Sure, they also say that it would be “completely wrong” for the authorities to impose much greater regulation on the industry, but still, this is almost an official spokesentity for the banking industry describing how their have been morbidly incompetent.

As as yet another Bush-era mess, the final collateral damage, beyond social cohesion, solidarity may be the rule of law:

Volcker Says Fed's Bear Loan Stretches Legal Power

April 8 (Bloomberg) -- Former Federal Reserve Chairman Paul Volcker questioned the central bank's decision to rescue Bear Stearns Cos. with a $29 billion loan, saying it was at ``the very edge'' of its legal authority.

``The Federal Reserve has judged it necessary to take actions that extend to the very edge of its lawful and implied powers, transcending in the process certain long-embedded central banking principles and practices,'' Volcker said in a speech to the Economic Club of New York.

(...)

Volcker said the Fed's loan may send investors the wrong message.

``The extension of lending directly to non-banking financial institutions -- while under the authority of nominally `temporary' emergency powers -- will surely be interpreted as an implied promise of similar action in times of future turmoil,'' he said.

Volcker said the modern financial system has ``failed the test'' of the marketplace. When asked whether he predicts a ``dollar crisis,'' he said, ``you don't have to predict it, you're in it.''

Get ready for the next lurch downwards, the same sorry excuses to bail out the losers that brought us this mess, more pain and tragedy for ordinary citizens, and more institutions utterly destroyed.