Maldistribution of wealth is the issue at the root of all of our problems, including, believe it or not, the passionate rift here on dailyKos. If we fail to stop and reverse the flow of capital, and thus power, from the middle and lower classes of this country to a few uber-rich, we will fail in our most faithful attempts to address other issues such as climate change, out-of-control military spending, public and private debt, erosion of constitutionality and the rule of law, the economy, media irresponsibility, etc.

Henceforth, we progressives need to evaluate every policy decision in terms of whether it continues the flood of wealth upward or truly provides net value for the middle class. (Perhaps it is more aptly called "downward.") At the very least, we need to understand the forces which can cause a person passionately to hold opinions very much at odds with our own. Assuming their goals are the same as yours—progressive, Democratic—they are likely neither trolls nor fools.

I am re-publishing this diary on the encouragement of several kossacks who thought its exposure suffered from having been published during the SOTU. It with some embarrassment that I re-publish a rescued diary. I hope this does not offend anyone. The response to the original convinced me that it might serve the site to see this again.

A couple of weeks ago, mem from Somerville celebrated the Boston Globe selection of Elizabeth Warren as their Woman of the Year. Embedded in the short diary is the hour-long lecture Ms. Warren delivered in June 2007 as part of the UC Berkeley Graduate Council Lectures which inspired me to write this diary.

Relying on her own work as well as that of Jacob Hacker, Prof. Warren has identified, quantified, and analyzed the single largest threat to the financial, political, and spiritual health of our republic—what she calls the "hollowing out" of the middle class. Listening to her thoughts has given me a fresh template for viewing current debates. I was amazed at the subtlety of many of the mechanisms by which risk and expense are shifted from the wealthy, and from common funds, onto the middle class. Talk of refunds for college expenses, for example, doesn’t begin to counteract the hundreds of tricks being employed to concentrate financial power in fewer and fewer hands.

Realizing that many kossacks will not have an hour to devote to this enlightening lecture, I took the time to listen and summarize. I write up the lecture in detail at the end of this diary. I invite you to read it through, because spending time with the details is essential for a solid intuitive feel for the forces we must combat. But before getting into the nitty gritty, I want to mention a couple of things and make a few general points.

The Equality Trust: Unambiguous Evidence

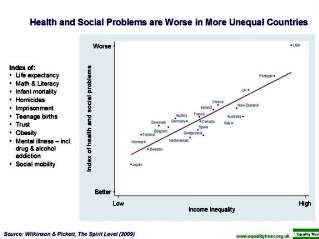

As I pondered writing up Warren’s lecture, I wondered if there was any solid data showing that inequality is damaging to a society. I don't want to be some naive, idealistic socialist or a foolish bleeding heart liberal. Heaven forbid. Almost magically, xaxnar appeared in an open thread, linking to his/her diary about the work of Richard Wilkinson and Kate Pickett. Thirty years of data collected from various countries has enabled them to show that greater equality within a society means better results in all of the following areas: physical health, mental health, drug abuse, education, imprisonment rates, obesity, social mobility, trust and community life, violence, teenage births, and child well-being. They further show that continued economic growth no longer brings real benefits to countries which are already wealthy. With reference to global warming, they argue that the creation of a sustainable economic system is also dependent on greater equality.

Chart courtesy of Equality Trust

[Sorry about the blurred chart. Here's a more legible view.]

Take my word for it, that's the "land of the freeper and the home of the brazen" almost off the chart in the upper right-hand corner. The data is amazingly consistent throughout the areas studied--the greater the wealth inequality within a country, the worse the problem under discussion. If we were a self-aware people, this situation would be an extreme embarrassment to us. We're negative number one in most categories.

And by the way, the problems associated with inequality are society-wide. This is not a call for rich folks to have a lower quality of life so that others can have a higher one. Greater equality in a society results in a higher quality of living for the richest person as well as for the poorest. Even GOP Jesus would support that.

Combating inequality has become a crusade for Wilkinson and Pickett, who along with Bill Perry established the Equality Trust in 2009 to get out the word and to work for greater equality. Please visit their website. Equality is a thing we can all work toward, independent of pressure on our government.

Why our fight over HCR is so difficult

I would like to use HCR as an example of what I mean by analyzing policy in terms of its relation to the issue of inequality. This also takes us to what I see as the real fault line causing so much angst on our website of late.

To put it briefly, over the last three decades, money going into our health care industry has gone increasingly to profits, and to enormous salaries at the top, rather than to actual care. We see this pattern in other areas as well: over a decade ago, a study found that only 25 cents of every dollar spent on education went to classroom instruction. In industry after industry we see this top-heavy pattern. So, our Congress was tasked with finding a way to provide health care for more Americans without offending the corporate donors who pay for the expensive campaigns, meaning without interfering with the flow of funds from the middle class to the very rich. The result so far has been an attempt to use tax money--which is middle class money--and money from middle class workers by taxing so-called "Cadillac" plans. Meanwhile, the health industry stands to become even further enriched, and further empowered to control the entire system, by the institution of mandates.

One result of this has been the impassioned, often fratricidal, debate on dailyKos. Chris Hayes wrote the clearest exposition of this that I have seen:

In pondering the answer, it's useful to distinguish between two separate categories of problems we face. The first are the human, economic and ecological disasters that demand immediate action: a grossly inefficient healthcare sector, millions un- or underinsured, 10 percent unemployment, a planet that's warming, soaring personal bankruptcies, 12 million immigrants working in legal limbo, the list goes on. But the deeper problem, the ultimate cause of many of the first-order problems, is the perverse maldistribution of power in the country: too much in too few hands....

The central and unique paradox of our politics at this moment, however, is that our institutions are so broken, the government so sclerotic and dysfunctional, that in almost all cases, from financial bailouts to health insurance mandates, the easiest means of addressing the first set of problems is to take steps that exacerbate the second.

Hayes employs an enlightening analogy, evoking a community suffering at the hands of a protection racket. Some of the poorer business owners are harassed and beaten when they can’t afford to make their payoffs. If a parish priest could stop the harassment by paying the protection money for the businesses, would he be doing good by preventing beatings or doing more harm by further entrenching the hoodlums terrorizing the neighborhood? It is a nearly impossible question.

Lest anyone read this as an argument for taking the long view, it is not. Hayes himself chooses the short-term solution with respect to HCR. May we model our behavior more on that of a person willing to take a decision at the same time he is willing to clarify the weakness of his position.

Almost everyone here wants to combat climate change, put people to work, and provide health care to folks. Some of us feel the most skillful policy is to accomplish what is doable even if it means further concentrating wealth and power; others of us feel that wrenching power and wealth away from those who have a stranglehold on our government is an over-riding concern, rendering the brutal compromises on health care unacceptable. I am grateful for the passionate, involved people working on both sides of this question.

The coming collapse of the middle class: Higher risk, lower rewards, and a shrinking safety net.

Now, on to Prof. Warren’s analysis of the societal changes over the last three decades which have led to increasing concentration of wealth in the hands of a few. If this is getting too long for you, please skip down to the boffo closing.

I wanted to start by talking about what I think is the single most important economic shift of the second half of the twentieth century in the United States, and that is that millions of mothers poured into the full-time paid work force. A woman in 1970 who had a sixteen-year-old child was less likely to be in the work force than a woman in 2003 who had a six-month-old child at home. It was a profound shift in America. The median family in America, married couple family in America, went over a thirty-year period—median, middle--from being a one-income household to a two-income household.

Along with most of us, Warren’s guesses as to the effects of this change would have been largely wrong.. The effects have been right in front of us, but we have failed to notice many of the mechanisms even after the fact. She would have guessed that families would move away from the suburbs closer to their place of work, as no mother of a six-month-old would commute over an hour to work. She would have been wrong. Her second guess would have been that families would be very wealthy:

They’re going to have lots of savings, no debt, and plenty of vacations. They’re going to be secure, they won’t have a lot of bankruptcy, there won’t be a lot of default, nobody’s going to be dealing with debt collectors.

Looking at a single generation, 1970 or so to about 2005, Warren now demonstrates that what has occurred is almost precisely the opposite of what one would have expected. All dollar amounts are corrected for inflation.

All graphs may be found in PDF format here.

First graph: See the second Fig. 1

Income went up for married couples , but income for a fully employed male is actually $800 less today than his father made a generation ago (median earnings). This flat or decreasing income for the single worker bucks the trend of the previous seventy years. Thus, all the increase in income was a result of a second worker in the work force. Still, it appears so far that the income of the average family has increased. Unfortunately, the devil is in the details.

Savings went down over this time period: The single-income family in 1970 was putting away about 11% of their take-home pay.... By the year 2006, you’ll notice the line goes below zero. This is a concept only Alan Greenspan would love: negative savings. The American family today puts away nothing, and frankly, has been putting away nothing for the last five or six years. There is nothing there. There is no savings.

So, savings didn’t go up the way I predicted. But something went up. And that would all be debt.

See figure 4

Choose any type of debt and you’ll see much the same picture: revolving debt (credit card), consumer debt (car loans, pay day loans, etc.), or mortgages. For example, revolving debt as a percentage of annual income: 1.4% in 1970 up to 15% in 2005.

Think about what that means. That means that over the last thirty years, in terms of a shift, the family spent everything that mom’s income added to the family fisc, spent everything they used to save—that 11% that they used to put away, and went into debt another 15% of income on top of that. They spent it all.

So, what did they spend it on? Ms. Warren’s inner nerd was excited to learn that between the Commerce Department and the Labor Department, she could find the answer to this question. Going back for over a century, one can study alcohol consumption, cracker consumption, rugs, cars, etc. To aggregate the data with stability with respect to such factors as age and family composition, Ms. Warren analyzed data for a family of a mom, a dad, and two kids. She compared the numbers in 1971 with those in 2003. The results are surprising, adding even further to the picture of a fragile middle class.

See figure 3.

Believe it or not, we spent 32% less on clothing. Probable explanatory factors--discount stores, imported clothing (think slave wages), and more casual dress. Well, what about food, especially with the family eating out more with mom at work, with the specialty items from around the globe, with bottled water? The 2005 family spent 18% less on food. Well, again we have discount stores and razor-thin profit margins, less spent on meat, and many other contributing factors. Okay, must be appliances that are eating up our consumer dollars—microwaves, expresso machines, popcorn poppers. This is what critics of our overspending lifestyle (Robert Frank and Julia Shore) would tell us. Well, try 52% less on appliances. Per car cost of owning a car has gone down by 26% (we keep cars an average of two years longer and repair costs have dropped significantly). Spending on furniture went down by 30% in a generation. Electronics went up, but only by $300. Dog food went up. Baby food went down. Cigarettes went down. Liquor went up. Dry cleaning went down.

The point is, there is a wash or a negative in terms of ordinary consumption.

We are not so much the overly consuming society we often see ourselves as. So where did the extra spending go? Well, let’s start with a 3 BR 1 Bath house.

See Figure 6

And there it is. In inflation adjusted dollars, a 76% increase in what a family spends on a mortgage.

Mortgage rates are lower than thirty years ago, but the higher price of the house more than offsets the difference.

The median-sized house did grow slightly in this period: it grew from 5.8 rooms to 6.1 rooms, and on average this median family either picked up a second bathroom or a third bedroom, but not both.

So what about the macmansions and the obligatory granite counter tops, etc.?

All that tells us is that the new housing market has shifted from the entry level house, which is what was being built in the 1950’s and 1960’s, to on average when you buy a new house today, it is your third to fourth house purchase. That is, you’ve moved up and moved up until you could afford this bigger house. In other words, housing is not being built for 70% of American families; it’s being built for the top 20% of American families. That’s what we see when we see new construction.

So today, they are about 50% more likely to be in a house more than 25 years old, and have all the attendant expenses for maintenance. But, just looking at the mortgages, 76% more.

Health insurance. Warren looks at her standard family, loading the dice by giving the family good health and an employer who sponsors health insurance. Apples to apples comparison of employer-sponsored health insurance between 1970 and 2004: 34% more. Cars: while expenses per car went down, the family with two workers owns on average more cars. Child care, a non-existent expense in 1970 has gone up by whatever percentage you want to put on it—Ms. Warren calls it 100%. Finally, taxes.

What happened with taxes is that, progressive tax system, as mildly progressive as it is, the first dollar that the second earner earns is taxed after the last dollar of the first earner, so it means that the tax rate for this economic unit has gone up by about 25%.

So there it is--downs and ups. And I hope there are two things you notice about the downs and ups. The first one is: the downs, frankly, are all smaller purchases than the ups are, and that’s bad news. And the second is, the downs are all flexible purchases, that is, lose your job, get sick, have a tough month with various expenses, you cut back on the downs. Don’t buy appliances this month. You know, cut back on food.... But look at those other expenses. Those other expenses are big, fixed, relentless expenses. So this gets to what I think of as the heart of what my research is about.

See figure 5, fixed costs as a share of family income

She looks at this from her commercial lawyer perspective—if this were a little business, is it becoming more or less fiscally sound?

In 1970, the single-earner family brought in around $44,000, out of which $19,560 was left for discretionary spending after fixed expenses were taken care of. In 2005, the dual-income family brought in about $73,000, out of which only $18,110 is left for discretionary spending after fixed expenses. The earlier family is spending about half of its income on fixed expenses, whereas the family today have committed 75% of their income to these relentless expenses.

You’ll notice, the math we’ve done here, the two-income family, the mom, dad and two kids, the prototype of the family that is supposed to be working in America, the one that’s supposed to making it all, by the time they pay their five basic expenses, they have less money left over, fewer total dollars, than their one-income parents had a generation ago.

Looking at it as a commercial lawyer, viewing each family as a business, one would conclude that the family of today will go broke a lot more often than the family of the 1970’s

...because they have so much less flexibility, so much more debt. They are much more deeply leveraged and are going to have a lot harder time economically.

And in fact, that is what has happened to these families.

That’s the economic side of it—the income and expenses and how they contribute to higher risk. But the risk is even higher than these numbers suggest.

From the point of view of income, the family today relies on two incomes to meet its necessary expenses. This means that, if the risk of unemployment had stayed exactly the same over these thirty years, then the dual-income family of today faces exactly twice the risk of not being able to make the mortgage payment. This family needs to bring in 104 checks to meet the mortgage payment as compared with the 52 checks required in 1970.

To make the same point from another perspective, the one-income family has a spare worker. If Dad falls ill or loses his job, there is an option of Mom finding work to meet the shortfall. She will earn less than a woman today, but every dollar she earns is additional, so that in combining this income with unemployment benefits, this family has a better chance of keeping the house. The family of today not only lacks an extra worker, but they are also already fully budgeted, leaving them nowhere to go.

Making matters worse, the risk of losing one’s job has not stayed steady. In The Great Risk Shift, Jacob Hacker has analyzed a family’s chances of a 20 percent or greater drop in income.

How about health? They now have double the chance that one of the two workers will be in a car accident. But his family now faces additional risks on the health side. The odds they won’t have health insurance have gone up. Also, the world of health care has changed in the last 30 years.

In 1970, for a non-ceasarian childbirth, the mother stayed in the hospital for 5 days after the child was born. For a caesarian, the stay was 10 days. In 2006, it’s 24 hours.

How have we made gains in hospital efficiency over the last thirty years? It’s send home sick people.... In the trade it’s known as send them home "quicker and sicker." They save money by letting the family provide nursing care instead of the hospital.

And so today we witness the spectacle of my mother-in-law, a woman in her 80’s, where someone’s trying to show her how it is that she can wash a tube and rinse things out and give injections. My sister-in-law was asked to do this when my brother had some surgery. We’re going to train the family...

So, if someone gets sick, someone else will have to take off work to take care of them. You’re not going to get this nursing care. It’s just another way to get one more push on income. If a child or a grandparent gets sick, a generation ago there was someone at home to care for them. Today, it often means that a working parent must miss work, often resulting in loss of a job. Today, an illness in the family has a direct effect on income.

The child gets sick--I read these stories over and over in my bankruptcy files--the child gets sick; mom stays at the hospital with the child until she loses her job. There are income effects now for any illness anywhere in the family.

We can continue multiplying these consequences—more risk of events which have more dire consequences. What are the odds of spending $10,000 in the ER compared with a generation ago? One more significant one that she hasn’t quantified yet—insurance has changed.

Insurance itself has changed in terms of how much of the medical cost is actually covered. We now have floating around in America, is just, I don’t know what else to call it except faux insurance: people who think they are insured until they actually get sick.

She mentions the announcement by a state official in Utah that everyone is insured. It turns out, the Utah insurance covers everything except hospitalization, specialists, prescription drugs, supplies, etc.

So all of this is being pushed back on the family.

Changes in jobs, changes in health insurance, changes in health care. Finally, the special risks facing families with children. Two points here—this is how it works for the iconic family of two parents and two kids. Imagine how it works for a single parent and two kids.

She refers to Hacker’s work on percentage increases in volatility in income by family type from 1970 until 2005. For a single person without children, a significant volatility of 35%, single with children is in the 40’s, married without children gives 75% increase in volatility, and married with children goes to 95% increase in volatility over the last generation.

Also, increases in housing costs for families with children vs. families without. We find a 50% increase in housing costs for a family without children, a 100% increase for families with children.

I’ll tell you how I read this chart. Families are buying schools. Families without children don’t have to buy schools, so they can buy from a wider pool of homes.

A five point increase in third grade reading scores between two side-by-side municipalities in Boston suburbs that are otherwise matched for access to public transportation, ... sidewalks, crime rates, racial composition—everything--translates into tens of thousands of dollars of differences in housing prices.

A study in San Diego found that parents would rather live near a toxic dump than in an area where they thought the schools would be under-performing. Parents are buying schools.

What’s happened to the American safety net for these families?

Personal safety net, the part you build yourself, has already been covered--less savings, more debt, higher risk, less flexibility, more people without health insurance than ever before.

In the 1970’s the uninsured person was an unmarried male, no children, 23 years old. Today modal is a 35-year-old married person with two children.... In 2001, 1.4 million people lost their health insurance. Of those, 800,000 earned more than $75,000 a year.

The people who have lost health insurance, who have lost that part of their safety net, are increasingly among the middle class.

Pension plans—the shift between the defined benefit plan and the defined contribution plan, meaning you put in money and you take the risk as to whether you will outlive your money, vs. the defined benefits plan, which is you’ll get a certain amount of money until you die. We’ve moved very much from the latter to the former, which means higher risk of losing the safety net.

Those are on the personal side. If you take a look at the public side, we’ve had the same kind of erosion of the safety net.

Unemployment benefits as proportion of income are not nearly as high as they were thirty years ago. What we pay for public education has eroded sharply.

In 1970, it took twelve years to educate a child to go forward into the middle class, or so parents said in a Gallup Poll.

Twice as many people in America by 2002 believed that the moonshot landing was faked...than believed you can make it into the middle class in America without a college diploma.

It means the launch, what parents have to do to get the next generation into the middle class, has shifted from something that everyone pays for (high school) to something that only the families with children pay for.

In 1970, almost no one sent their children to pre-school. Experts recommended against it. Today, the specialists recommend two years of pre-school. So, to launch into the middle class today, a child needs 18 years of education, a third of which is paid for by the individual family. Just as to costs—City of Chicago launched a pre-school program with some tax dollars in it. The tuition was larger than the tuition at the University of Illinois.

How have families responded to this?

Percentage of families filing for bankruptcy in 2001—unmarried men, unmarried women, and couples with no children all filed for bankruptcy at a rate of a little over 7 per 1,000. For a couple with children, the rate more than doubles to 15.3 per 1,000. For women head of household, no husband in household, the rate is 23 per 1,000. There aren’t enough unmarried men with children to give a statistically significant number.

Families with children are under enormous financial stress. I watch them, I study them, from the bankruptcy end of the spectrum, which is where they end up, and let me tell you a little bit about why they file for bankruptcy. Ninety percent of those families file for one of three reasons: job loss, medical problem in the family,...or family breakup—either a death in the family or divorce in the family.

Nearly half the families have two of those three, and 20% have been hit with all three.

More children live in homes that will file for bankruptcy this year [2007] than live in homes that will file for divorce.

This has been true since the late 1990’s. Why don’t we know more people who are filing for bankruptcy? There’s an enormous stigma attached:

Don’t use the word.

About 85% of the families that are filing for bankruptcy are hiding it from their own parents, from their siblings, from their best friend, and in some cases, from their own children.

They make up stories—have to move in to take care of a family member—are moving across country to get a better job.

This has enormous implications for the poor. Middle class families under enormous economic stress have fewer resources to give, and they have less appetite to give. A middle class that looks like this has less room to bring the poor families up into the middle class.

There’s no place for the poor to go, and not much help coming from the middle class today compared to a generation ago.

I fear we’re moving from a three-class society to a two-class society. America has always been one of those perfect distributions--some poor, some rich, and a big, big solid middle class, stuck right there in the middle. Americans identify with the middle class. It’s part of our democracy. It’s what gives us our political stability. It affects our economy, it drives our economy, it affects our self-identity. It affects who we are in this world. And I fear that what’s happening, that what these data are about, is that we’re actually going to see a larger upper class--we’re seeing it, not just the rich rich but the sorta rich—the ones who have the same jobs, bringing in two incomes, who don’t get sick, who don’t lose a job, ...who don’t divorce, who don’t have a death in the family, who don’t hit any of life’s bumps—they stay with the upper group....And then the rest is just one long trail of underclass that stays on a constant debt treadmill—sometimes it’s a little more, sometimes it’s a little less, but they’re never out of debt, never any real economic security. I could change my metaphors. People constantly living on the edge of a cliff—some falling over, some scratching back up a little—but they’ll never enjoy the kind of security that, for the first three-quarters of the century we associated with being middle class. I worry about what that means.

That threatens the fabric of our country.

In summary

Warren has found that in one generation, the typical working family has added a second adult to the work force and is more in debt than ever. Families are spending all of the second income, plus what they would have saved 30 years ago plus adding debt. Where is the money going? It is not going to increased spending on consumerism as many like to argue. Rather, it is going to required fixed expenses of living a decent life--housing, health, taxes, education and necessary transportation. People are spending a greater percentage of their income on much older, similarly sized, houses than a generation ago. People are spending more on lower quality health care than a generation ago. People are spending more on education with a lower chance of their children succeeding than a generation ago.

Why is the increased spending buying less? Obscene profits is surely one of the sinks. Where the middle class family lives on the edge of bankruptcy, especially the single parent family, a small percentage of Americans is more wealthy than ever before. Families are going bankrupt all around us, and most of them are not talking about it.

Call it socialism if you like, but decent societies expect mortgage lenders to include as part of their mission supporting a stable housing market. Instead, they have focused on schemes for siphoning off middle class equity into the hands of a few. Any healthy culture shares the education of the next generation. Our culture has created a profitable, top-heavy educational industry supported at great expense only by families committed to educating their own children. If claiming to be Christian involves anything more than killing Muslims, surely it involves caring for the sick and dying. Our health care industry has become yet another scheme for enriching a few while showing little commitment to actual health and a dismal record of compassion.

So, industries are growing obscenely wealthy off the ordinary needs of citizens. At least with heroine, the pusher has to make a person become addicted to the product. With housing, health care, and education, the "addiction" is inherent; everyone needs these things.

The net result is that, compared with a generation ago, Americans are putting more energy into work, spending less time with their children, and living in much higher danger of bankruptcy than ever before. In other words, America looks more feudal and less free, economically, than just thirty years ago. We are not caring for our children, we are not providing housing for ourselves, and we are not getting the health care we need. We are number one in most of the wrong ways. If these trends are not reversed, our future is bleak.

- You can go to Equality Trust for action ideas.

- You can analyze every policy proposal as to whether it truly brings relief to the shift of wealth and risk or simply moves middle class tax money around in creative ways that do nothing to interrupt the concentration of wealth.

- You can educate yourself and others to see more clearly the shifts we are undergoing and to recognize the price we are paying.

Two comments from the original diary

For further reading of someone who has also focused on this issue, particularly with respect to the political and social instability and violence likely to result if increasing numbers of the middle class fall into poverty. NBBooks:

I think you will also be very interested in It Could Happen Here, Bruce Judson's Blog.

Posts from the ‘Economic Inequality’ Category

* Discussion with WNYC’s Leonard Lopate on January 3rd, 2010

* Troubling signs... on January 3rd, 2010

* Income Inequality Threatens America’s Basic Economic and Political Systems on October 29th, 2009

* Will Extreme Economic Inequality Lead to Terrorism? A Chilling Moment on NPR’s OnPoint on October 20th, 2009

* New Income Inequality Data: Surprising and Frightening on September 29th, 2009

And finally, a great summary from papicek

to sum it all up...

This huge economic expansion the leadership (of both parties) was so proud of was almost entirely funded by absorbing the median family's savings and then by sending that family into debt.

There's your history, writ large.

Final plea for compassion

I believe the painful rift on dailyKos, immaturity and incivility aside, springs from a very real and understandable difference of opinion with respect to challenging strategic choices. Perhaps we can be more forgiving of ourselves and one another if we accept that many policy decisions today necessitate a nearly impossible choice between fixing an immediate problem or attacking structural problems. In most cases, the choice to go either way can be justified as both ethical and practical. We are caught on the horns of a dilemma; here's hoping we can become more compassionate, appreciative, and supportive of one another as we engage these issues in good faith.

Update: Our country is failing to address this problem in large part because we are hiding it. Our media takes a lot of the blame, but another factor is the embarrassment and shame associated with poverty. This comment by wavpeac made me sob. I include a part of it in the diary in hopes we can look more clearly at what folks are going through. If we can be more aware that this is life for a lot of people, we will more likely be able to notice when our friends are in need, be more sensitive about evaluating people on the basis of wealth, and be MOTIVATED TO DO SOMETHING about his kind of suffering instead of indulging in ego battles on the internet.

He then quit paying child support for the next two years. This was the beginning of my night mare.

At any rate, the effect was this.

1. dreaded birthdays. Could afford to buy gifts for people.

2. sometimes had to pay larger fees like for shut offs because I was always balancing groceries, mortgage and utilities. This sometimes meant I got shut off and had to pay extra fees. This is embarrassing.

3. Dreaded christmas

4. Could not go out to lunch with folks at work...so embarrassing to explain why.

5. couldn't return gifts to friends who gave them to me. Gave home made gifts and services...tried to put a good face on it, but my friends had money.

6. couldn't join people when invited to do things like "go swimming" or go to the zoo, or the amusement park.

7. couldn't share in discussion about this kind of stuff.

8. constantly felt less than everyone around me.

9. couldn't even afford cleaning supplies...stuff like mops and brooms went by the way side. I used bleach, vinegar, and dish washing soap for almost all cleaning and this was a good thing.

10. quality of food...fruits and veggies most expensive. Kids loved fresh fruit...I tried to put it first in the budget but it was a struggle. I knew we could eat less meat.

11. clothes. Hand me downs...salvation army. Hard to look like a million bucks...but I did okay. It took a lot more thought than today.

12. Doctors appts. I couldn't afford the deductible most of the time.

13. computers and electronics. I live in a middle class neighborhood. Kids in hs were expected to have a computer. My kids did not for several years. It was very difficult for them to use the lab at school only open and free early before school starts. If there were changes that needed to be made on a paper teachers often would forget that the boys needed the lab. They didn't care. Time was way different for them than today for my last two who have a computer in the home.

14. having to take a day off because I couldn't afford the gas to get to work.

15. no money to move (first and last months rent, deposit if I wanted to walk away).

16. pet...we had a dog when all this happened. It was impossible to afford the fees for shots, and registration. We skipped it but felt so guilty.

17. plates on cars...big stress every time it came around.

18. Car insurance. There were times I let this slide because I chose to buy groceries. How awful to criminalize the inability to pay for insurance. This would put me in the high risk category when I would be able to buy it again. Despite never having an accident, my fees would be triple.

I am just saying that emotionally the toll is so much more than simply going without a few things.