In her diary today nyceve reports that HHS has finalized it's new rules limiting Health Insurance Rate Hikes, in that diary she mostly focuses on debunking the claims led by AHIP that such hikes are necessary by pointing out that Health Insurance Companies are among the most profitable in the country, and in fact the best paid CEO in the country doesn't work for an Oil Company or a Technically Company - it's the CEO of United Health Care.

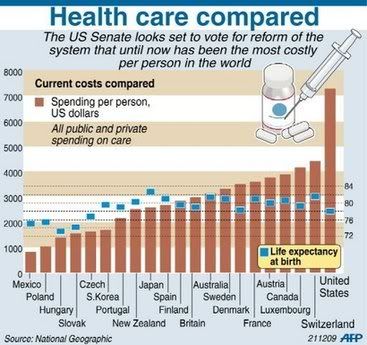

We all know that America Health Care Costs are completely out of Wack.

Instead of repeating that fight, which is about as difficult to prove as the wetness of water I'd like to start a new one.

In their criticisms of the ACA, many have argued that it did not contain sufficient "cost controls" and have said that the only way to implement such controls would have been to create a "Public Option", which in the final draft of the legislation was replaced with a Non-Profit Option.

But there are Cost Controls in the ACA and Kathleen Sebelius has just proven it with this pronouncement.

“Health insurance companies have recently reported some of their highest profits in years and are holding record reserves,” Ms. Sebelius said. “Insurers are seeing lower medical costs as people put off care and treatment in a recovering economy, but many insurance companies continue to raise their rates. Often, these increases come without any explanation or justification.”

Federal health officials proposed the 10 percent threshold in December. The insurance industry criticized it as an arbitrary test that could brand a majority of rate increases as presumptively unreasonable. But the administration rejected the criticism and insisted on the 10 percent standard in the final rule, issued Thursday.

The final federal rule as of NOW is that any Health Insurer that proposes rate hikes greater than 10% are going to have to Justify It. Unlike the ridiculous claims of the likes of Gingrich, this is not any kind of "Soviet Tyranny" - it's simply deterring a pack of filthy ravenous thieves from running off with grandma's life savings, and possibly her life as well.

The downside of this is that in truth, whether Insurers do manage to justify the hike or not - there's isn't much the Federal Government can do about it other than give advice to the states on how to better recognize when they're being scammed.

Under the new rule, federal and state officials will review rates in the individual and small-group insurance markets. In effect, the administration said, large employers can take care of themselves, as they are more sophisticated purchasers and have more leverage in negotiating with insurers.

Federal officials acknowledged that they did not have the authority to block rates that were found to be unjustified. But they said many states had such authority, and the federal government is providing $250 million to states to strengthen their capacity. A small number of states, opposed to the federal health care law, have turned down the money.

Just as many State Rights advocates would have it, the power to control and limit the ability of insurers to gouge their customers begins with the States. On in this case, since they've refused the funds that would help them unravel the InsuranceCo double-speak, the Red States are the ones that will be left most vulnerable.

Two years ago when Blue-Cross/Blue Shield attempted to raise their rates by 39%, that hike was stopped and significantly reduced after State Regulators analysed their books.

Anthem gained notoriety last year for trying to impose a 39% increase only to be exposed for incorporating bad arithmetic into its rate filing. In October, many of its customers faced a 20% rate hike instead. The 16.4% increase Anthem announced at the beginning of this year, now reduced to 9.1%, comes on the heels of an annual profit of $2.9 billion for the insurer's parent company Wellpoint, Inc.

"If you buy health insurance in California, your only hope right now is that publicity and politics might convince some executives to scale back the rate increases, at least for a few months," said Heller. "Even with all the attention on these overwhelming rate hikes, Anthem customers are still facing an approximately 30% premium hike in less than a year. That is unsustainable and unacceptable."

Marking the line at 10%, and providing better resources for State Regulators to pound the bully pulpit and reduce these hikes is effective. But it's still not enough.

The California Department of Managed Health Care (DMHC) declared Anthem Blue Cross's impending May 1 rate hike "unreasonable" for at least 120,000 Californians, but acknowledged that state law provides the agency no power "but to publicly express our disappointment that Anthem Blue Cross didn't lower the rates as we requested." According to the non-profit Consumer Watchdog, policyholders will be forced to pay unreasonable premium increases that appear to range between 16% and 25% and include increases to the policy deductibles as well. Legislation passed by the California Assembly Health Committee Tuesday -- AB 52 (Feuer) -- would allow both the DMHC and the California Department of Insurance (CDI) to regulate health insurance premiums and prohibit insurers from imposing excessive rate hikes such as the Blue Cross increase taking effect on Sunday.

"When a regulator finds that a rate hike is unreasonable but can't do anything about it, we obviously need more regulation," said Consumer Watchdog Executive Director Doug Heller. "If the only consumer protection is the ability of a regulator to be disappointed, then we have no protection at all."

This confirmation that Blue Cross is imposing an unreasonable rate hike comes two days after Blue Cross parent company Wellpoint announced that its profits for the first quarter of 2011 were nearly $1 billion, up 6% over last year.

So the power, at least in California, to block outrageous rate hikes currently rides with the fates of AB 52.

Under current California law, the insurance commissioner is not authorized to block excessive rate hikes from taking effect. Both Anthem Blue Cross and Blue Shield, along with other insurers, have aggressively opposed efforts in California to regulate health insurance rates. This year, a bill – AB 52 (Feuer – Los Angeles) – has been introduced that would give the insurance commissioner power to reject excessive health insurance premium hikes. Insurers are likely hoping that their sudden decisions to reduce rate hikes will defuse the mounting pressure for real rate regulation in California

The proposed reform legislation,AB 52, would require insurance companies to get permission before implementing any hike and would allow the insurance commissioner to deny or modify rate changes determined to be excessive.

Like Roaches that scurry when you shine a light on them, Anthem/Blue Cross has been ducking for the nearest cover whenever their ridiculous rates have been revealed - and with that the new HHS Rules make that spotlight even brighter. Now with AB 52, they're going to have to come to the State Regulators and ask permission for such rate hikes first, not after they've announced them.

But there's another card that the Federal Government has to play. Within the 15% Medical Loss Ratio requirement that is part of the ACA for Insurers who wish to participate in the Health Exchanges in 2014 - is a Rebate Requirement for those who NOW, TODAY - have been exceeding that MLR for current clients.

Several provisions regulating insurers were added, including a requirement for an insurer to provide rebates if its share of premiums going to administrative costs exceeds specified levels and a general prohibition on imposing annual limits on the amount of benefits that would be covered.

This may be just one reason why Blue Cross was willing to cut it's proposed 16.1% rate hike back to 9.1% earlier this year as that move would prevent them from having to pay rebates in 2014. It's also a clear reason why AHIP and other Health Insurance lobbyists have thrown their weight behind repealing the ACA so that these limits and controls will go away with them before the 2014 deadline hits.

You see, it's all about profits - and these companies won't give them up until their pried from their cold, dead, actuarial tables.

As of now, we are yet another step closer to doing exactly that.

Vyan