In my previous life, not so long ago, I taught introduction to Microeconomics as I worked my way through grad school in Economics. Intro Micro is one of my favorite classes to teach, because it contains some of the core analytic tools of economics, allowing people to take situations which happen in their lives every day and comprehend how we can influence events in our lives to positive outcomes.

During the first week of lecture, I would discuss two ideas: what an economic model is, and one of the most basic economic models, the circular-flow model. Both aspects are useful for understanding the Great Recession, so if you would follow me past the dKos fleur-de-lis...

A model is a construct -- it's a way of looking at the world which approximates what is going on, so that we can ignore the overwhelming data which would prevent us from seeing underlying patterns. That is, the act of creating a model is the act of deciding what to ignore. That's why the selection of a model is sometimes an inherent selection of values.

I liken economic models to maps -- different models are good for understanding different aspects of our economic life in the same way that different maps are good for helping us solve different problems. An historical map of Europe, for example, might help us to understand how their current borders evolved, but it would be utterly useless for helping us find a house in Poughkeepsie. And that map of Poughkeepsie would be valueless for someone looking to plot great-circle routes from New York to Japan for an airline. The fact that a model doesn't apply to a given problem is not a knock on the model; it's a statement of what the map is good for.

Models are delimited by assumptions. These are statements which the model relies on, whether or not they are true in the real world. Getting back to our map analogy, assumptions are the equivalent of:

1) Where the borders of the map are

2) What the scale of the map is

3) Whether the map highlights roads or topography or climate zones, etc.

You can see that this model of the earth we call a map is capable of many different types of analysis depending on the assumptions used to build it. Economic models are no different. And you can see where someone who wanted to deceive someone else about, say, property lines could simply use a map which shows the wrong information or shows information which is subtly related to, but different, from the discussion at hand.

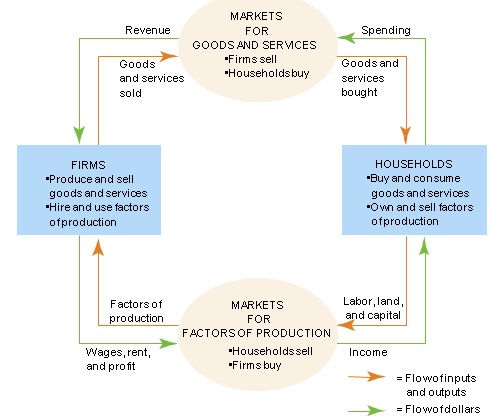

This is an introduction to one of the most basic models economists have access to, the circular-flow model. It is a model of how economies work in general. It is the equivalent, therefore, to something like a globe, a map of the world at the most general level.

Here we go:

(Image borrowed from an old edition of N. Gregory Mankiw's Principles of Microeconomics. Used without permission for eleemosynary purposes.)

In this model, there are basically two major types of organizations -- households and firms. Households provide labor and own capital. Firms hire labor and rent capital.* Firms produce; households consume.

Before we get into this model, I need to acknowledge some decisions we've made about what to include and what not to include in our first version of the economy. Firstly, where is the government? We'll add it and talk about it later. Secondly, most households are both firms and households. Fair enough; we can talk later about how that modifies our thinking. Finally, we aren't discussing fraud or force in this model. This means that it is not nearly as useful for describing economies or sectors of the economy which are characterized by lots of fraud or force.

Does this mean that the model itself is fraudulent? That's actually a great question. Models themselves are just models. But they can be presented in a fraudulent or honest fashion. Honest presentations of models highlight the assumptions which underlie them and are careful to discuss where those assumptions might not be good approximations. Just like an honest map tells you where it is and what sorts of thing it highlights. One of the most effective ways to dishonestly use a model is to use one which has as one of its assumptions the pattern you're seeking to support with the model. You see this a lot with people who use economic models that assume full employment to prove that something is good for employment.

Ok, so -- we have this model, and it lets us see some patterns. In particular, we see that the economy never particularly starts anywhere. An economy is a constantly moving flow of goods and services from firms to households. In addition, money is a mechanism which moves counter to the flow of goods and services.

Let's track a couple of common transactions and see how they work in this model. In the first transaction, Brian pulls off the interstate and buys a candy bar at the corner gas station for $1. Brian goes to the market for goods and services, finds a place where he can buy a candy bar, then gets the candy bar. A candy bar travels from the "firms" box to the market and then to Brian in the "households" box. Meanwhile, Brian pays a dollar -- a dollar travels from the "households" box to the market and the to the gas station in the "firms" box.

Amanda looks for and then gets a job as waitstaff at the local restaurant, for which she is paid $5 an hour plus tips. So Amanda, a member of a household, goes to the market for factors of production. She finds a buyer for her labor, the restaurant. She then provides her labor to the restaurant. In the other direction, the restaurant goes to the market for factors of production and uses its money to purchase Amanda's labor.

Let's talk about a few extensions of the model and explain why we didn't include them in this picture. For example, firms purchase both goods and factors of production from other firms -- there are intermediate goods used in production, and firms can rent land from one another as easily as from households. Why didn't we include extra loops for firm-to-firm transactions? Two reasons -- firstly, all goods are eventually consumed by households, and secondly all factors of production are eventually created by households. So we don't get any additional information about how the economy works by adding extra loops. All we do is complicate the diagram. Another example is households which are firms. We can still see how that would work by mentally separating the household and firm functions in our heads, even if they're combined in the real world. And in the same way, goods and services are exchanged for factors of production, even if it takes place without any money changing hands.

Hokay, that was fun. Now let's explain something interesting -- what's the difference between an economy which has full employment and our current situation in which there are people who want to work but cannot find jobs in this model? In both cases, people go from households to the market for factors of production to find opportunities to sell their labor. However, in our current economy, some people who want to sell their labor can't. Firms, however, are able to find as many laborers as they need for the amount of goods they're selling. Since fewer people are working, firms are producing less stuff. So households are consuming less.

This suggests an interesting question -- how is it that firms increase in size at the same rate that households increase consumption? This seems like sort of a tricky thing to get right, that both sides would be expanding at exactly the same rate such that neither are left hanging. It seems like it would be easy to stay at any given equilibrium, but it would be wrenching to move up or down from 5% to 9% unemployment equilibria. Of course, this is true; it took a massive financial collapse to move us from 5% to 9% unemployment, and we seem pretty stuck here now, with a Catch-22 of firms being unwilling to expand without improved markets, and households unwilling to consume more without more income.

I hate to leave everyone hanging, but I'm going to. What has changed as a result of this model? We're now asking the right question. Rather than asking, "What the heck happened?" we asking, "what has changed such that we moved to a different equilibrium in the long term, and what can change such that we move back in a reasonable period of time?" This is the central question of Keynesian economics, and it's the circular flow diagram that allows us to ask it intelligently and systematically.

I hope this is a useful way of looking at the economy. Please feel free to ask followup questions in the comments. One of the great tricks of economics is learning when to apply certain models, and how to modify them slightly to answer the question you want to learn about.

*For this discussion, "labor" is human time and energy spent producing something of value. "Capital" is an item which is used to make other things. Capital can be as complicated as a skyscraper or as simple as a socket wrench. It's what it's used for that matters. Since all firms are ultimately owned by households in some fashion, all capital is similarly eventually owned by somebody.

Update: Hey, wow, community spotlight? It's incredibly flattering to see myself at the top of the page there. Thank you so much!