If you haven't been trapped by the CNBC noise machine, you should be aware of the on-going credit crunch. After the Dow Jones Industrial originally peaked on July 19th, it began a steep descent that became horrendously dangerous within days. To put it in this perspective, by the third week of the crisis, the DJIA was at one point down for six days in a row. On the first day (August 9th), it had plunged 387 points. On the sixth day (August 16th), in hindsight the markets seemed determined to go for, at the least, a mini-crash. At one point that day, stocks were down about 400 points, only to close flat after the soothing words of Ben Bernanke could be heard on the other side of the wall, "I'm here for you." Since then, stocks were moving at a bubbling rate that has, until now, been consistent. After reaching a record high, it seems that this was more the result of overshooting on a euphoria that was simply unfounded. Welcome back to late July.

Once again, this coming week may turn out to be a real downer for the stock market; a nascent downturn, one not too different from the one we saw during the week of July 23rd-July 27th. So it is known, I have said repeatedly (namely my last two diaries) that the stock market is heavily divergent from the greater economy. Neverthless, the main observation is that the rally ended more dramatically than you may realize, which at the least should indicate that all is not well.

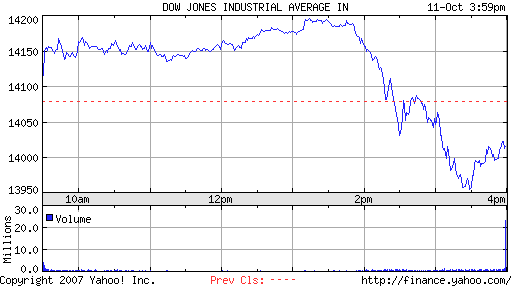

Last Thursday, the DJIA was looking to shoot the moon once more, as it was up about 125 points at 2 p.m.. Just when everything seemed right, it took an unexpected dive and resulted in a 250 point reversal only 90 minutes later. This was hidden by the actual loss of about 125 at 3:30.

On Friday, stocks were not all that impressed by the retail sales. When the more recessionary aspects of the retail numbers were included, such as the fact that food and energy sales were up while demand for more discretionary items fell, the +0.6% jump in retail sales was stripped to -0.1%. Recessionary, indeed, as it means consumers are focusing priorities involving human implications. In short, stocks rose purely on the headline numbers, but were kept under the lid by the warnings.

Monday was really depressing. Oil breached a record high of $86 on Monday afternoon, a spike of about $2. Eighty-six! Wow! This contrasts with economists who believed oil would begin to drop after hitting $80, but this has clearly not been the case. This, too, is recessionary, as it means consumers will have less disposable income in the following months. The DJIA, for what it's worth, was off 170 at one point, but closed down about 110 instead. Still pretty lousy.

The momentum cleary became more negative toward the end of last week.

Earlier in the day, Citigroup announced its earnings plunged 57% and on top of that....

Citigroup Inc., the biggest U.S. bank, said mortgage delinquencies and consumer lending will deteriorate for the rest of the year after earnings fell 57 percent in the third quarter.

Citigroup had its biggest drop in two months in New York trading after Chief Financial Officer Gary Crittenden said on a conference call that borrower defaults are ``accelerating.''

LINK

This indicates the credit crunch is not only persevering, despite the happy talk, but is destined to actually worsen. It has also been well forecasted that hundreds of billions of dollars in ARMs will reset in the next few months, threatening foreclosures on an epidemic level.

Still yet, the Dow Jones Industrial Average is showing a stark divergence from the Dow Jones Transportation Average. Even though the DJIA rose sharply, the DJTrans is flailing around its August lows. This suggests the economy is considered to be in worse shape than would seem based on "stocks." Companies in charge of moving capital goods are less bullish than the more irrational industrial indices. When this occurrence happened back in 1999 and 2000, the story did not end very well. More on this here.

As a disclaimer, I am NOT an economist nor a financial adviser. My only purpose is to make observations, not suggestions about how you deal with any assets you own.

All of this news is backdropped by state data that are extremely recessionary, such as the drop in sales tax receipts and floating unemployment. It is well known that the government unemployment numbers are underreported, as they only count workers who not only continue to look for a job, but are still receiving unemployment benefits. The unemployment rate is naturally higher than what is reported. Nevertheless, keeping the data consistent, even the government numbers indicate that unemployment is catching up.

So, here is the reality check. Job growth is starting to decline and in California the number of unemployed has surged 17% from November 2006 to August 2007. This is a trend, since unemployent rose in 5 out of the last 6 months. A comparison between 2007 and previous recessions suggests the strong correlation between unemployment surges in California and nationwide recessions.

In addition to California, other states not even considered in the center of the subprime crisis are showing sharp rises in unemployment...

New York is pretty intimidating.

What about Illinois?

Missouri has served as a strong indicator of recession, according to this study this study by the Philadelphia Fed Reserve.

More signs that all is most certainly not well, brought to you by yours truly.