A few of you have gently chided me for not doing any Countdown diaries since the oil prices have gone down. While the giddiness and glee demonstrated by many in the traditional media and elsewhere invites little but ridicule, as demonstrated by this graph below, prepared for the Oil Drum, some serious questions have been asked in various threads and deserve answers.

So, beyond the semi-glib answer that nothing much has in fact happened in the oil markets in the past month (after all, the recent decline is quite smaller, in percentage terms, than several others in the past couple of years), here are a few points worth making.

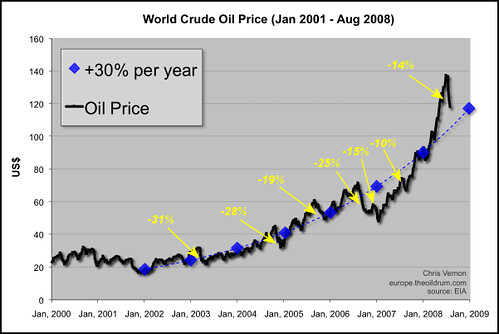

An installment of the Countdown to $200 oil series

"It was speculation and the bubble has popped"

"Such small variations in demand or supply cannot explain such price changes"

"What about the Iran war premium - that's speculation right?"

"Demand is down (in the US), prices will go down back to normal"

"Asians will reduce their demand too"

Many don't agree with my assertion that speculation has little or nothing to do with the run-up in oil prices, and consider that the brutal price increases, followed by just as brutal price decreases, cannot be explained by fairly small changes in supply or demand figures.

Let me try to explain again why, in today's conditions, small variations have precisely such consequences.

In a market where supply is plentiful, balancing the market will be done by supply adjusting, ie the price will be such that just the required volume of oil is extracted to fulfill demand, and no more. In that case, competition between suppliers plays in full, and the price will the be the marginal cost of supply, is the cost of the most expensive barrel needed to fulfill exactly demand. All cheaper producers will get that same price (and will make a nice profit the cheaper their costs are), and those that are more expensive won't produce. In such circumstances, variations in demand (or new supply coming online) can only cause price to move slowly along the production cost curve, and bigger price movements usually come from "above ground" factors, ie geopolitical crises that include a risk of major disruption of supply.

But if you move to a market where supply is fully used to satisfy demand, you enter a whole new world. In that case, if potential demand still increases, there is no supply in the short term to fulfill such demand, and the absolute requirement for physical balance of the market translates (beyond using stocks, which can only be temporary) into a need to destroy demand, ie for some potential users to forego using oil. As we all know, oil is really convenient, and we are all unwilling (and, in many cases, unable) to stop using it. And yet the demand destruction needs to happen. In the short term, that requires prices to go high enough to convince someone to stop using the stuff, either because s/he can't afford it, or because s/he chooses an alternative which is less convenient but cheaper and, at such level of saving, worth the hassle. In such circumstances, short term price movements can and will be quite violent. In fact, any event that disturbs supply, any news that shows that demand was higher than expected, or supply less than hoped, or that suggest that demand will be higher than thought, or supply lower than expected, will push prices up immediately (and the opposite news, down, of course), because thee news translate into a unbalance between supply and demand and a bigger need for demand destruction (conversely, a lower need for such).

- So, a pipeline blows up in Nigeria - bam, 200,000b/d of (high quality) oil off the market, demand destruction is needed!

- Ben Bernanke suggests that a recession is unavoidable - psssh, prices go down as a slower economy will translate into less demand for oil, and thus less demand destruction will be required;

- Oil storage goes up - aha, demand was lower than we thought (or supply higher) in the last month, and there will be less need for demand destruction in the next one!

- Bush agrees to direct talks with Iran - bam, the war premium goes down, as the probability of an oil-supply-endangering conflict (which would cause a massive and brutal need for demand destruction, unless strategic storage is tapped) goes down.

In fact, in the past month, these was a succession of news that all went in the same direction. In the same week, Bernanke was extremely bearish on the economy, oil stocks were higher than expected, and talks with Iran happened. Each of these took about 3-4% each from the price of oil, bring the price down by more than $15 in 3 days.

And any time this happens, speculators are wrong footed and they need to close out their positions, which usually reinforces temporarily the underlying movement (haha! so there are speculators! And they push prices around! Well, yes, there are speculators - but, for the most part, they follow the market rather than driving it. Any price overshoot is usually temporary. And they do provide valuable services, by bringing in liquidity to prices - and by providing willing counterparties to those that want to buy hedges - you know, like airlines that buy futures or options for their supply over the next few months or quarters at prices to protect themselves - and their fares - from yet higher prices).

:: ::

One point that needs to be made again is that demand destruction in the US (or even in Europe, where it is hapoening too) is not enough on its own to bring prices down, because it needs to be larger than the supply growth in the rest of the world to limit the requirement for further demand destruction and price rises, given that production is still largely stagnant. And the problem is that demand is not growing just in China and India, thanks to rapid growth, it is also growing massively in oil producing countries themselves (Saudi Arabia, Iran, Russia, Venezuela), which often subsidize gas and which can afford it given that they have a natural hedge against (the subsidy gets bigger when oil prices are higher, ie when their own income is bigger, and the income growth is larger than the subsidy growth for those that export any volumes). In fact, most of the demand destruction happens in price sensitive places, like the poorest oil-importing countries (but they weren't burning much of it anyway), and the rich world (which can still afford oil, but consumes lots of it). But we can't be sure it happens fast enough to actually cause prices to go down because of what's going on in the rest of the world.

Anything that encourages demand reduction elsewhere (like lower subsidies) helps to bring prices down, but it's by no means obvious that we've reached price levels that are sufficient to cause overall demand stagnation in the face of flat or quasi-flat production. Oil producers have little or no incentive to boost their production if they expect prices to keep on creeping up (and they can help that trend by, precisely, investing less), and it's not clear what substitutes are available in any meaningful volumes.

So, at this point, I'm still happy to continue my "Countdown to $200 oil series" and see no reason why the recent lull in prices would be a sign of a serious trend change in the market.

In fact, I'll say again that our energy policies should focus on one thing first and foremost: demand reduction. Any reduction in demand that we manage in excess of what market forces would (precisely) force us to do will get prices down, and will save us a lot of money - and the smartest demand destruction is the permanent kind, that brings savings every month and every year rather than one-offs like giving up a trip.

We have to reduce our demand. Let's do it in an organized way rather than a panicked, haphazard, inconsistent way. And that's where government can help, by providing longer term pespective, informing citizens, pushing infrastructure in the relevant direction, and bringing up standards that apply to all equally and guide individual behavior in the right (Energy Smart) direction.

Price mechanisms work, but they are brutal, hurt the poor the most, and cause unnecessary disruption to economic activity, and pain to many. And they are fickle, as the current volatility (which, as I explained above, is likely to remain) causes rapidly changing signals which prevent decisions from being taken.