Total US GDP is roughly $14 trillion dollars in total size. Because of this size it simply won't reverse on a dime -- especially considering the length and breadth of the current recession. Instead gradual change is how to measure progress. On several fronts this week we saw the news continue to signal that the worst of the recession is probably behind us. However, that does not mean we have clear skies ahead

Perhaps the most important news release was a continuing decline in initial unemployment claims.

In the week ending June 6, the advance figure for seasonally adjusted initial claims was 601,000, a decrease of 24,000 from the previous week's revised figure of 625,000. The 4-week moving average was 621,750, a decrease of 10,500 from the previous week's revised average of 632,250.

First, here is a chart of the more recent moves in this indicator.

Notice how the 4-week moving average (the solid line) topped out about 6 weeks ago and has since been moving lower. This is the longest period of decline in the last year and a half (the length of the chart). Combine that chart with this one:

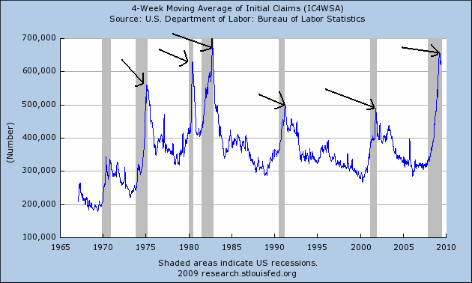

And you see the strong possibility we have seen the worst of the job cut news. The reason why this is important is illustrated by the following chart:

In the last five recession initial unemployment claims have topped out right at or slightly before the official end of the recession.

A second piece of good news occurred on the retail sales front:

The U.S. Census Bureau announced today that advance estimates of U.S. retail and food services sales for May, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $340.0 billion, an increase of 0.5 percent (±0.5%)* from the previous month, but 9.6 percent (±0.7%) below May 2008. Total sales for the March through May 2009 period were down 9.7 percent (±0.5%) from the same period a year ago. The March to April 2009 percent change was revised from 0.4 percent (±0.5%)* to 0.2 percent (±0.2%)*.

Notice how the retail sales chart breaks down into three important points.

1.) Sales fell off a cliff at the end of last year.

2.) The last five months they have fluctuated around 0% change.

3.) The year over year number appears to be bottoming as well.

There was also good news on the consumer confidence front:

U.S. consumer confidence rose to a nine-month high in June, a survey showed on Friday, but inflation gauges showed worrisome signs of price increases that could slow any recovery from the longest recession since the Great Depression.

June's consumer confidence reading failed to surpass the level reached last September, when the spectacular failure of Lehman Brothers sent the world economy into a tailspin.

The Reuters/University of Michigan Surveys of Consumers said its preliminary index of confidence for June rose to 69.0 from May's 68.7. That was slightly below economists' expectations of a 69.5 reading, according to a Reuters poll.

For the third straight month, the overall consumer sentiment reading was at its highest since last September's 70.3.

"It's good news but not great news," Hugh Johnson, chief investment officer at Johnson Illington Advisors in Albany, New York, said of the June confidence data.

We have now had four straight months of increases in this number. The main cause for concern is we still have not gotten above the levels of last September. But we are close.

The apparent continuing indications that the worst is behind us there is little reason for celebration. As I have outlined in previous articles there is little reason to think the recovery will be robust. However, that does not mean we should look a gift horse in the mouth.