This week we saw several more pieces of data which add up to a sign the economy is bottoming. Let's go to the data.

First we have the Federal Reserve's Beige Book:

Reports from the 12 Federal Reserve Districts suggest that economic activity continued to be weak going into the summer, but most Districts indicated that the pace of decline has moderated since the last report or that activity has begun to stabilize, albeit at a low level. Five Districts used the words "slow", "subdued", or "weak" to describe activity levels; Chicago and St. Louis reported that the pace of decline appeared to be moderating; and New York, Cleveland, Kansas City, and San Francisco pointed to signs of stabilization. Minneapolis said the District economy had contracted since the last report.

Note the key phrases "the pace of decline has moderated or that activity has begun to stabilize, albeit at low levels." This phrase is in tune with several pieces of month over month data which show stabilization at low levels.

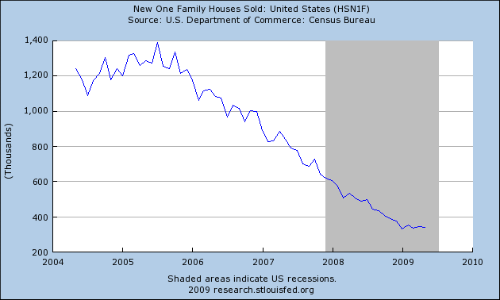

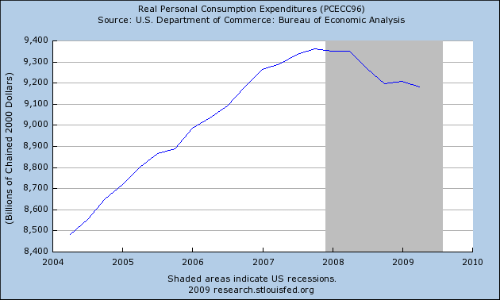

The point to the above charts is the free fall has stopped and the economy is now moving sideways.

In addition we continue to see improvement in initial unemployment claims.

From the Department of Labor:

In the week ending July 25, the advance figure for seasonally adjusted initial claims was 584,000, an increase of 25,000 from the previous week's revised figure of 559,000. The 4-week moving average was 559,000, a decrease of 8,250 from the previous week's revised average of 567,250.

...

The advance number of actual initial claims under state programs, unadjusted, totaled 507,464 in the week ending July 25, a decrease of 78,111 from the previous week. There were 376,123 initial claims in the comparable week in 2008.

While the number of adjusted claims increased this week, notice that the 4-week moving average decreased (again). Also note the general trend of initial unemployment claims is still lower.

Finally, note the unadjusted number dropped by 78,111 this week. This is in addition to a drop of 90,000 last week for a total two week drop of 160,000. This adds further evidence to the fact that employers are slowing their pace of lay-offs.

The Chicago Purchasing Managers Index also increased:

Month-to-month change in the Chicago area has stabilized for new orders, very good news reflected in a 3-1/2 point rise in the Chicago purchasing managers' index to 43.4 in July. The new orders component jumped 6.4 points to a nearly break-even 48.0. A 50 reading would indicate no change from the prior month, so the 48.0 reading indicates only marginally weaker order levels in July compared to June. There is some encouragement also for employment which rose more than 6 points to 35.3 as it hopefully also continues to climb to 50.

This report is in line with the slow but steady rise in the other regional indexes:

And the ISM index:

While industrial production is still negative, recent reports show a slowing decline as well.

Finally, we got the preliminary 2Q GDP report which showed a contraction of 1% (-1%).

Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- decreased at an annual rate of 1.0 percent in the second quarter of 2009,

(that is, from the first quarter to the second), according to the "advance" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP decreased 6.4 percent.

There was good and bad news in this report. The primary bad news was personal consumption expenditures decreased by 1.2%. This indicates consumers are still very concerned about the future and are therefore being extremely careful about what they spend their money on. However, business has slowed their investment contraction. Nonresidential investment dropped 8.9% from the first quarter compared to a drop of 19.5% in the 4th quarter and 39.2% in the first quarter. In addition, residential dropped 9% in the second quarter compared to drops of 25.9% and 36.4% in the 4th quarter of last year and the first quarter of this year respectively. While these numbers are still negative it's important to remember they are part of a series which was incredibly bad a few months ago. To expect a level of improvement into positive territory at this stage is very unrealistic. Instead, gradual improvement is far more likely -- which is what this report indicates is occurring.

In addition, we are almost through earnings season. More and more businesses are stating they see the economy stabilizing:

A quick review of second-quarter corporate report cards so far this season shows a growing number of companies willing to venture - on the record -- that they've probably seen the worst of the Great Recession.

That doesn't mean they see a big rebound in the months ahead. Some do, many don't. About the closest Corporate America comes to consensus at this point is that the economy has stabilized. But that hardly means things are truly on the mend.

"While we would all like to say that the economy is improving, we've really seen simply stabilization," Greg Hayes, United Technologies' chief financial officer told investors on a post-earnings conference call.

So -- where does this leave the economy overall? I'm on record as saying we'll start seeing growth somewhere between the 4th quarter of this year and the second quarter of next year. It appears the economy is on track to make that mark. To expect the economy to immediately move into 3%+ growth and 5% unemployment after what we've been through is highly unrealistic. In short, we're getting near the end of one of the worst recession we've seen in our lifetimes (the other being the double dip recession of the early 1980s). There's going to be some incredibly tough roads ahead. Growth will be slow -- in the 1%-2% range -- for initial stages of the recovery. Unemployment will still be in the 7-8% range by the end of next year (if not higher). The point is there's no reason to think the recovery will be a gangbusters economy.