The Wall Street Journal has an interesting article out today discussing utilizing unused TARP funds to pay down the deficit and the potential for either spending cuts or freezes across the board. The real question is why the sudden concern about the deficit during a time that would normally be ripe for running deficits to act as stimulus? The Journal supposes it's national politics:

White House Chief of Staff Rahm Emanuel is pressing for substantial spending cuts to go with any tax increases to try to avoid the "tax and spend" label that has bedeviled Democrats, according to administration and congressional officials.

I, however, think that is very unlikely, as Republicans will use the tax and spend label no matter what (heck they used it when Clinton was running a surplus). What I see is that the administration is getting very concerned about the dollar, interest rates, and China.

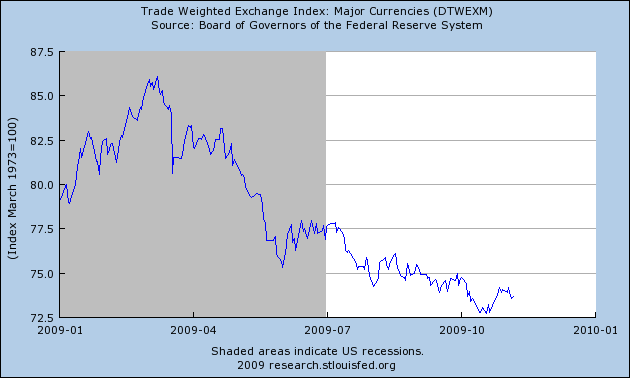

First, ever since the markets (and economy) earlier this year, the dollar has been in free fall.

This free fall of the dollar has corresponded with the reflation in commodity prices (ie oil) and leaves us in a precarious position as higher oil prices become very constraining on economic growth. The fall of the dollar also means that we have to pay relatively more for commodities than countries whose currencies exhibit relative strength. This makes our commodity dependent industries less competitive globally while also making it very difficult for consumers to both pay for higher commodity costs (gas and food) while also paying relatively more for imported goods. The falling dollar is likely a direct result of our large deficit spending and thus a prime reason why the administration is looking to cut the deficit even in the face of continued economic decline.

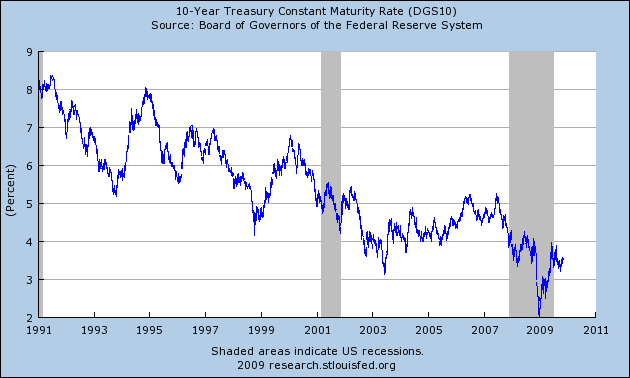

The belief in our ability to pay back borrowed money with dollars that have similar value to the ones that were lent has a direct impact on interest rates, which are currently still hovering at extremely low levels.

You can see from the graph that even with an almost doubling off of the panic induced lows earlier this year that the 10-year interest rate is still at near historically low levels, which has enabled us to borrow money for our spending very cheaply (and made the decision to rack up huge deficits much easier). The problem lies in that spike and the loss of confidence in the dollar, which plays a direct role in the rate someone is willing to accept over a 10 year term in order make a real return on their investment (ie principal+interest > inflation). The problem we are facing is that it is quite likely that interest rates will rise in the near future as investors demand a higher rate to offset potential inflation risks (inflation in the loss of value of currency sense), which greatly impacts our ability to finance our debt plus include any additional deficit spending.

This is quite troublesome, as Obama's Budget never has the 10-year interest rate exceeding 5.2% all the way through 2019. This is quite concerning, as during the 90's (which were not exactly known for high interest rates) rates were well into the upper 5's and 6's for the bulk of that decade and that was during a time in which we did not have huge deficits projected out into eternity. What this means is that if interest rates rise substantially above the projected 5.2%, then our debt service payments rise dramatically and crowd out other federal spending initiatives (because further deficit spending at that point will only cause interest rates to rise more in concert).

So, where is China in all of this. My guess (and it is really just a guess at this point) is that China has begun to put real behind the doors pressure on the administration to reduce our deficits/strengthen the dollar, with the implied (or direct) threat that they will not continuously show up at our auctions to buy our debt at low rates anymore. In my opinion this type of scenario is the most likely one to explain the Journal article above, as Obama (and his economic advisers) know full well that now is not the time to start worrying about balanced budgets.

In essence, we may be screwed as we face one of these two scenarios:

economic recovery based on deficit spending = higher interest rates that kill the recovery, or

economic stagnation due to a premature withdrawal of stimulus in an effort to keep interest rates low and the dollar "strong" (the one likely benefit of stimulus withdrawal is a steep fall in commodity prices, which seem to be entirely driven by speculation again as hedges against the dollar with all of the liquidity that is around from the stimulus).