It's been breathtaking (in a bad way) to watch the media - and especially a few prominent liberals - turn on the Obama administration this week. The amount of media backlash - both within the traditional outlets and the blogosphere is too numerous to encapsulate. But one article stands out for me:

Will The Unemployment Disaster Be Obama's Katrina?

That the analogy Huffington makes to Katrina is both inept and ridiculous goes without saying. But it underscores, for me, a rather surprising short-sightedness and lack of understanding of the American economy, its current state of health (or sickness), and what can realistically be accomplished by any President regardless of party. Much more below the fold.

A Car Analogy

Since most of us drive cars and, if we do not, are at least familiar on some level with the essential elements of a car, I'd like to use it as an analogy.

A car is made up of many different parts. The "heart" of the car is the engine itself. If your transmission goes but your engine is fundamentally sound, you can repair or replace the transmission for some cost and the car will function again as expected. The same idea applies to brakes and tires and other supportive parts of the car itself. But if it's the engine itself that is broken, you have a wholly different problem. Repairing the transmission on a car with an engine that doesn't function gives you a new transmission in a car that still won't move.

Now take the analogy even further. Let's say, for the sake of argument, that engines themselves are incredibly scarce. If you can't replace the engine in that car, nothing you do to its supportive systems will get it moving. It's a simplistic analogy, I know - but it's one that I think is an apt foundation for discussion.

Toto, We're Not In Kansas Anymore

Our economic engine has been on the brink of failure for years. The approach that the American government has taken has been to shore up those systems that, if left unattended, could add to and speed the decline of the engine itself. But we haven't been addressing the core fact: The engine is failing. And it's only a matter of time before all the non-systemic, non-core repair work we've been doing fails to keep that engine running.

The Census Bureau conducts an economic census every 5 years. They track broad sectors of the economy, as follows (from the 2002 Economic Census Summary Statistics by NAICS):

Mining

Utilities

Construction

Manufacturing

Wholesale Trade

Retail Trade

Transportation & Warehousing

Information

Finance & Insurance

Real Estate & Rental & Leasing

Professional, Scientific & Technical Services

Management of Companies & Enterprises

Administrative & support & waste management & remediation service

Educational services

Health Care & Social Assistance

Arts, entertainment & recreation

Accommodation & food services

Other services (except public administration

These sectors, collectively, represent the engine of the US economy. I would argue that some sectors - manufacturing in particular - are more important in the bigger picture than are others.

So let me use the housing boom as a representative example. The chart below tracks mortgage interest rates over the past decade (from MortgageNews Daily):

You can see that interest rates started downward at the beginning of the Bush administration and reached a 10-year low in 2004. Not coincidentally, that was the same time that financial deregulation was in full swing - a fatal combination in my opinion. But I digress.

Come back to the list of economic sectors. The construction, transportation & warehousing manufacturing, wholesale trade, finance & insurance, and real estate & rental & leasing sectors were all materially involved in the housing boom - they were front-line sectors that benefited from the low interest rates and high housing demand. And many secondary sectors benefited as well - retail trade (one must furnish one's new house), management of companies & enterprises, administraive & support & waste management & remediation services (new houses and developments mean new demand for waste removal), educational services (more houses means more people who require more schools), health care & social services, accommodation & food services, utilities and a plethora of other services all benefited from the increased demand for housing, driven by the low mortgage interest rates.

There's just one problem - the housing "boom" was driven by artificially low interest rates. This, coupled with financial industry deregulation and a proliferation of immoral and ridiculous "loan products" caused unbalanced inflation not just in the housing market, but in all the ancillary markets primarily and secondarily involved with the construction of houses.

Reality Sets In

(Note: it's actually very difficult to find concise by-sector data on the US economy)

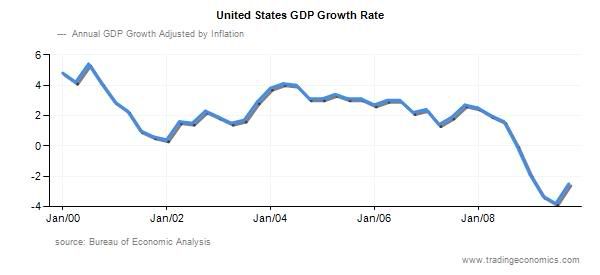

So I found this chart interesting - from Trading Economics.com:

What you see there makes sense (at a very high and simple level) given what we know today. GDP was trending downward (and had been for years, dragged down by decline in the manufacturing sector) through 2002. and then VOILA - mortgage interest rates hit their lowest level in decades, the housing boom is kicked off, primary and secondary market sectors start improving, and we're off to the races... until reality sets in.

And the reality is that people - and countries - can't endlessly spend money they don't have buying things they really don't need without there being some kind of consequences.

Bailouts & Stimulus

There are two extremes of thought about what should have and should still be done with respect to managing the US economy through this recession. One extreme says that we shouldn't bail out companies that went around the bend and got involved in risky business and/or were otherwise financially unsound. That extreme doesn't buy the idea of "too big to fail", and it doesn't buy the idea of the government creating jobs to help buoy the economy. The other extreme believes that we have to bail out the biggest companies and help keep employment - however anemic - alive while we figure out the rest of the puzzle and right the ship of the American economy.

I look at it pretty simply. Somewhere, there is a bottom to this economy and that bottom is the extreme of how far it can fall. Picture it like this - you're driving your car at a high rate of speed. Your path is inevitable - you're driving towards the bottom of the economy. One extreme, visually, has you driving that car off of steep cliff. Once the earth has disappeared from under your wheels you're in a free-fall. Your car is subject to the laws of gravity, and you pitch nose first towards the ground below you (the bottom), and that bottom is looming large. You smash nose first into the ground, and your car is destroyed and its occupants are either instantly dead or in the process of bleeding to death, broken at the bottom of that chasm.

The other extreme seeks to cushion the blow as you get to the bottom. As you're driving, you hit a downward slope. You pitch down that slope, and it's scary - and then you level off for a period of time until you pitch down another downward slope. You keep doing this until you come to the bottom. You're jangled, no doubt, but your car is still intact and its occupants are still alive. They're shaken - worse for the wear - but not bleeding, broken, and dead or dying. Your car's alignment is undoubtedly trashed and will need repair, and your car's occupants will definitely need time to recover from their ordeal.

So bailouts - while unsavory and definitely unearned by the companies who benefited are, to me, a necessary evil. I could launch into a long discussion of the failure of the past Administration and, to this point, of the current Administration to put into place the safeguards that prevent these situations from arising in the future - but that would be beside the point of what I'm getting at.

What matters in this whole discussion is THE BOTTOM. The bottom of our economy has, historically, been a point that we reach - either via pitching off the cliff and lying broken and dead on the ground or via a ramshackle and frightening downward-slope journey with less devastation at the end. And it's traditionally at the bottom that we rise again and things begin to recover. Industry starts to pick back up, and employment again starts to flourish.

Historically.

And now for a dose of reality

The real question of the day is whether or not we have anywhere to recover TO. As I've laid out in this diary, in very simple terms, the US economy has been kept afloat by smoke and mirrors. The unnatural and devastating inflation in the housing economy prior to the recession masked the real, systemic problem.

People, corporations, and our government have been living beyond their respective means for far too long. What's been going on under the covers is a story of erosion in our economy. Jobs have been outsourced to cheaper labor markets. The US' dominance in manufacturing has been flagging for years as goods production has moved to Asia and Mexico and other developing countries where the cost of labor and production is cheaper. The middle class - long supporters of and workers within the manufacturing sector - is disappearing.

Yet concurrently, prior to September 2008, our standard of living and all the purchases that go with it have been INcreasing. A decent house big enough for your (I'm referring to the all-inclusive "you" and "your", here) family to grow and improve wasn't enough - you had to have a McMansion and lease a luxury car that inflated the appearance of your standing while realistically depleting your financial resources. The amount of stuff - most of it totally unneeded - that you required and purchased exceeded your ability to afford it. Government has behaved no differently, starting and perpetuating two wars which were unaffordable in reality with no discussion of or plan to address its cost. The concept of the family budget - and also the government budget - fell victim to a driving need to conspicuously consume.

And so where does that REALLY leave us? Simplistically, it leaves us with a deep need to reset. Our economy has already reset, even though we don't seem to realize it and the media largely ignores it. What doesn't seem to have sunk in is the fact that the economy we will eventually come back to post-recession isn't the same one that we had pre-recession.

And that includes the jobs economy.

And so, Arianna...

The thrust of the article linked in the intro to this tome of a diary is that the Obama Administration isn't stimulating enough. It suggests at some length that the President's economic team isn't up to the task of addressing unemployment and the larger economy.

That may be true - but it remains to be seen. What the article doesn't discuss is the concept of a reasonable level of unemployment and re-employment in the new, reset and realistic economy that we face. It's certainly not the employment levels we saw prior to the recession's true onset. That level, I submit, is absolutely unsustainable within the confines of hard, cold reality.

It's all well and good to beat on what's being done incorrectly and what's NOT being done (and there's plenty of ammunition for that beating)- but without the fundamental context of what's now realistic, any discussion of "jobs" has no foundation - no fixed point towards which we are working. No realistic hope of attainment. To hold the Obama Administration beholden to restoring employment to pre-recession levels is to build expectations to a level where they will undeniably be disappointed and unmet.

A second stimulus? Yeah, ok. I'm down with that, but only from the perspective of REALITY. A second stimulus is only another downward slope inserted to ease our ramshackle journey to the bottom. It can help preserve our bones and keep us from bleeding to death quickly, but it doesn't move the bottom any higher than it already is. By writing and publishing the article in the fashion that she did, Huffington adds to the illusion - or delusion - that somehow there's something that can or should be being done within the current economic reality that restores jobs and unemployment to pre-recession levels. And that's just setting everyone up for a fall and for failure. It's the ultimate strawman, and it's easy fodder for the opposition.

Raise the bottom

I'm not absolving the current Administration of its responsibility to our economy and the people who work within it. Far from it. I'm merely suggesting that Huffington's argument utterly misses the point and misses a big step that has yet to occur.

Raising the bottom will require so many things - all of which are complicated and which are going to be time-consuming. Health care reform - REAL health care reform - can help to raise the bottom. It can decrease the rate of inflation we are currently experiencing in healthcare costs, and that, in turn, can help improve the average family's retention of personal income and it can further help their ability to make needed purchases and their ability to save. We are hip-deep in that discussion, yet it's seemingly divorced from the broader economic discussion and how it contributes to "raising the bottom".

Energy policy is also going to impact where the real economy exists. Insisting on meaningful reforms to energy policy and instituting much needed regulation is one step. Further investing, as a nation and as a people, in the energy industry is another. Manufacturing decline has long been the gradual, pernicious drag on our overall economy and its commensurate employment. Investing in alternative energy leadership and production can help us raise that bottom more meaningfully than continually bailing out industries and companies that have, essentially, outlived their useful lives.

Re-regulating the financial industry, re-visiting trade policy, and always keeping a sharp and responsible eye on spending and the deficit contribute as well.

For me, the jury is out on the Obama Administration because there are so many things that have to happen to help us back to economic health. Health care reform has been FUBAR thus far. The messaging has been all wrong. Health care reform, energy policy, financial regulatory reform, etc. and so forth should always been couched, publicly, as to how it contributes to the overall economic picture and how reforms and regulations and policies benefit employment and each American's ability to thrive again in the US economy.

Endlessly flogging the Obama Administration for not creating more jobs is moronic. And worse - it contributes to the delusion that there's some mythical US economy that exists today that Obama can somehow work us back TO.