Because you just can't have enough spin, this diary looks at the various efforts by the government to halt the economic slide. It is written in a sort of CNBC style, and in doing so, completely ignores the government contributions which created the crisis. I'll leave that to the cynics.

I was not as successful as CNBC at ignoring results. I tried, but the stubborn-me keeps insisting that results can still play an important roll in determining if a decision was good or bad. If you are certain you will only get your information from CNBC, then you can safely skip those parts.

When I first heard Bear Stearns collapsed, I thought a football player had a stroke.

To me, the collapse of Bear Stearns marked the beginning of the current economic crisis. As long as you ignored the so-called prescient economic luminaries and just listened to the government, then this event was quite a surprise. Who would ever have thought real estate prices could also decrease?

With Bear's stock at $170 in 2007, everything was just fine. We know this to be true because any one of the numerous regulatory agencies would have said otherwise. The prior collapse of 2 hedge funds owned by Bear do not count because they are not regulated. There was no reason for the regulators to act all panicky and check on the overall health of the company; something like that would violate the spirit of self-regulation and undermine the entire regulatory system.

As it turned out, Bear Stearns was riddled with nervous clients, and when one started twitching, they all started twitching, and they began removing their money. Out of courtesy, Bear Stearns called the Fed and mentioned they had a funding problem.

The Fed understood, and like a good friend it rushed to help. Together, they called JP Morgan Chase and Bear was able to get rid of itself and it's disgusting clients by selling all of its shares to JP for 2 bucks a share. The government thought that was too good a deal and demanded that JP up the offer to $10. The government wanted a piece of the action for taxpayers and demanded some of Bear's valuable assets in exchange for $30 billion dollars of taxpayer money.

When the reality of the Bear collapse sunk in, Jim Kramer vented his anger in a scalding column on March 21, 2008:

That $30 billion from the Fed will turn out to be a small price to pay for a bottom in the stock market after the beating we’ve taken over the past eight months. We’ve been through dozens of false bottoms, but this time, with the Fed and Treasury basically saying they will do anything it takes to save the system, you finally have a floor that can hold the weight of America’s savings.

I have no idea who could have been calling all those bottoms, but for him to allude that the $30 billion the government paid for assets... ASSETS! might be worthless is near slanderous. The current value of those assets are $26 billion, and I am sure glad the government isn't trying to sell them for us because they surely will increase in value.

People like to point fingers, and some pointed them at the regulatory agencies. This is of course ridiculous because the regulators had in place strict voluntary compliance rules. Still, they stepped up to the plate and talked openly and frankly about accountability. Here is an exerpt:

No SEC models take into account "the possibility that secured funding, even that backed by high-quality collateral such as U.S. Treasury and agency securities, could become unavailable," Cox said in the prepared remarks.

Cox even prepared his remarks! The SEC was not to blame; it was their models. If that's good enough for Barney Frank, then it's good enough for us.

From March until the beginning of September 2008, we know the fundamentals of the economy were sound. Paulson and Bernanke even used my exact words in front of Congress. We know it was true because Congress has a special way to deal with contemptible liars, and there is no evidence that Hank or Ben were ever ignored.

Everything was so sound that in July 2008, there were a series of announcements by Paulson, Bernanke, and even president Bush that everything was especially OK at Fannie Mae and Fraudie Mac, and just to be sure, they were going to raise the debt ceiling by $800 billion in case a loan to them was needed... not that one was needed.

It was striking that with so much concern and support shown by the government toward F&F that they would up and fail... almost.

On Sept. 7, 2008, the head of FHFA announced it was going to place Fannie Mae and Fraudie Mac into conservatorship. This was not a typical case of severe corruption that the mortgage giants are well known for; this was due to the sudden realization that they had no more money!

In place of just loaning them the $800 billion, the government surgically removed the will to live from these institutions, and mainlined the treasury right into them. Experiments too gruesome to describe here are still being performed on them. One experiment was designed to rewrite mortgages for hundreds of thousands of people, and to date it has easily helped tens of people.

As if F&F were not enough trouble, exactly one week later Leahman Brothers filed for bankruptcy on the Treasury's busiest day - Sunday. It was not a case of nervous clients, but rather, they said, a case of nasty speculators trying to discover the true value of the company by shorting their stock.

The government was fearful they might try to sell toxic assets, which would set a market price for them and ruin everything. Hank held an open house for Leahman all weekend to see if anyone wanted a free Wall Street powerhouse. Nobody did, and the government put their foot down on lending money to banks. It was not going to happen again, and Leahman was history.

The government was very upset at the speculators, and punished them and everybody else by preventing the short-selling of stocks in most of the big companies. This had the effect of removing 50% of the liquidity of these stocks and it showed up in a graph of the stock market as a waterfall-like pattern. When the government learned that the Leahman failure was actually caused by a $1 bet between Mortimer and Randolph Duke over a new employee named Billy Ray Robinson, they felt terrible and rescinded their pledge of no more money for the banks.

In fact, they were growing concerned about the banks. The banks started behaving like everyone else and began not trusting banks. They were quite comfortable with their too-big-to-fail moral hazard arrangement, and they thought years of bribes and the millions they spent to rewrite laws had their status secured until the Leahman surprise happened.

This resulted in a phenomena that I have specialized in for years, and that is a liquidity crisis. A liquidity crisis often coincides during periods when there is no money. In the case of most of the banks, they had a liquidity crisis of indeterminate length, but unlike most people or companies, this poses no problem for banks because they know where money grows wild.

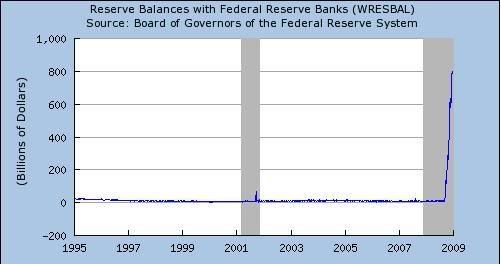

Always alert and ready to assist at an instant's notice, the Federal Reserve began manufacturing money in anticipation that the banks may desire some. This is indirectly illustrated in the following graph:

It's kind of interesting because mid-way along the graph in the shaded area denoting a recession, you can see a sharply pronounced spike that sticks out like a sore thumb. That was 9/11 and the Fed's response to the systemic shock it produced. Off to the extreme right, there is something very interesting; I have taught my cat to be fascinated with my printer when it is printing, and I believe that giant spikey line is from my cat ripping the paper out of my printer because it sure as shit cannot be the increase in cash made available to the banks. That would be obscene.

The same day Leahman was failing, Bank of America made quiet inquiries to the government, asking, "where's my bank, bitch?!!" The government, always ready to please, handed them Merl Lynch, as they say down south, and it also handed BofA money to make it look like they bought Merl.

Yes, they brought gum for everyone, and Citi had its beak open waiting to be fed Wachovia bank, but Wells Fargo snatched it up before the government could fully regurgitate the dead bank. Wells bought Wachovia's $812 billion in assets, and it's $448 billion in deposits for $15 billion. That's how numbers work in the banking world.

Citi was pissed and demanded an immediate $20 billion in cash, and another $306 billion in loan guarantees. The government handed them our money, but they forgot to ask for our t-shirts.

The oversight was understandable, because Hank and Ben were furiously drafting a 3-page document that was to chart the way out of this financial crisis for... at the most... $700 billion. Most likely not all the money would be needed, but even if it was, it would prove to be money well spent when considered against the alternative of worldwide economic catastrophe and shooting citizens dead in the streets.

This monumental emergency program was named TARP, which stands for Bailout Slush Fund. There was widespread belief that the money was going to be used to purchase troubled assets from the banks. This misconception stemmed from what was written all over the 3 pages Hank and Ben submitted, but they later clarified the matter and said that they were only talking about buying assets in the emergency program, and that maybe we read into it too much.

To date, only a little more than half the money has been used to purchase things we have no right in knowing, but that is consistent with the results so far, so things are on track.

The Fed cannot understand why the banks are not lending money. They have done everything to accommodate the banks, including a program to pay interest on excessive reserves that banks deposit at the Fed.

Some people question if a program that encourages banks to hoard cash is helpful in getting banks to lend money, but so far the Fed only says, "Please more sir! My English no so good."

When the graph above is shown to them, and they are asked for an explanation of where all that money on the right came from, they insist it is coming from Mouse's cat, and they expect that cat to cough up a whole nuther page for the new spike.